web3.GSEA Snapshot 2021 由 AppWorks 製作,有任何指教與建議,請 email 至 [email protected]。感謝以下 AppWorks 的朋友,在過程中提供的協助:Peter Ing (Co-Founder of BlockchainSpace)、Leo Pham (Manager of Access Ventures)、Hung Nguyen (CEO of Spores)、Tri Pham (CEO of Kardiachain)、Ben Minh Le (CRO of M3TA)、TN Lee (Co-Founder of Pendle Finance)、Lawrence Samantha (Founder of NOBI)、Eagle Su (Marketing Specialist of Zombit)

Jun is an Analyst covering both AppWorks Accelerator and Greater Southeast Asia. Born and bred in America, Jun brings a wealth of international experience to AppWorks. He spent the last several years before joining AppWorks working for Focus Reports, where he conducted sector-based market research and interviewed high-level government leaders and industry executives across the globe. He’s now lived in 7 countries outside US and Taiwan, while traveling to upwards of 50 for leisure, collectively highlighting his unique propensity for cross-cultural immersion and international business. Jun received his Bachelors in Finance from New York University’s Stern School of Business.

Founded in 2009, AppWorks is a leading startup community and venture capital firm built by founders, for founders. We are committed to backing the next generation of entrepreneurs in Greater Southeast Asia (ASEAN+Taiwan) and helping them to facilitate the region’s transition into the digital age. Building off the firm’s decade-plus of experience, AppWorks works closely with early-stage founders to achieve product-market fit, while helping growth-stage companies establish sustainable business models at scale.

Starting in 2018, blockchain was incorporated in the firm’s core mandate. We believe that the technology is currently driving a massive paradigm shift, opening up new disruptive and innovative opportunities for the next generation of entrepreneurs as the world transitions into the web3 era.

In 2021, blockchain entered a mass adoption phase. With the emergence of new innovative applications such as DeFi, NFTs, GameFi, and web3 infrastructure, an unprecedented number of new funds, retail investors, and users have flocked to the crypto world, creating a flywheel effect that has facilitated the formation of key web3 infrastructure that we believe will usher in a new era of large-scale commercialization.

“As the world decentralizes, will development vary between different countries and regions?” This is a question that we’ve mulled over years. With the accelerated development of blockchain, we recognize that, in fact, regional dynamics have become more pronounced. We found that in Greater Southeast Asia’s major markets, the confluence of different historical, economic, industrial, societal, and cultural contexts has resulted in crypto adoption taking different forms. The emergence of diversified crypto markets is driving growth in the region to meet different market conditions and leading to new business models and approaches in the industry that can be applied globally.

The following is an overview of our analysis and views on each major market in the region:

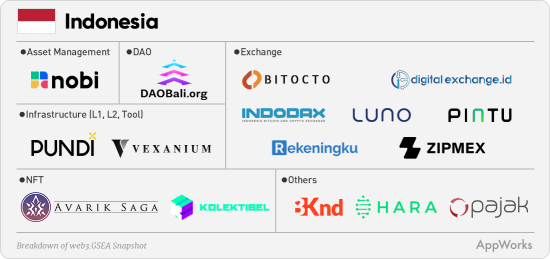

Indonesia: Crypto Investment Outstripping Public Equities

Indonesia, the world’s fourth largest population and the largest in GSEA, is estimated to have an unbanked population of 66%. Based on market size alone, Indonesia has become an important market for the development of blockchain. Indonesia is entering a financial paradigm shift driven by blockchain and cryptoassets, and overall development is trending towards exponential growth. According to statistics from Indonesia’s Ministry of Trade, during the first five months of 2021, more than 6.5 million people in Indonesia traded cryptocurrencies—far exceeding the 2.2 million who traded public equities—totaling US$25 billion in cryptocurrency transactions, compared to US$4.4 billion over the same period in 2020, representing year-on-year growth of 470%. With statistics like these, it comes as no surprise that cryptocurrency has become the most popular investment category among Indonesian retail traders.

Compared with other countries, the Indonesian government is relatively positive towards crypto. Since September 2018, a series of laws have been enacted, signaling the open attitude of the Indonesian government. The Commodity Futures Exchange Supervisory Board (BAPPEBTI) oversees cryptocurrency-related issues and has provided legal frameworks for licensing and trading. Currently, Indonesians can legally own and trade a total 229 different cryptocurrencies.

Indonesia’s crypto landscape is underlined by the rapid development and adoption of exchanges, wallets, asset management tools, and other DeFi applications. For example, Indodax, established in 2014, is Indonesia’s leading exchange with more than 4.7 million users. With increasing acceptance of investment in cryptocurrencies by the general public, new areas of development, such as investment platform NOBI, that provide asset management services that cater to crypto users will mark the next wave of growth.

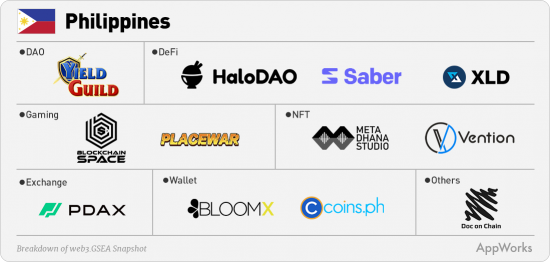

Philippines: Massive User-Driven Growth

In 2021, Yield Guild Games (YGG) broke out in the Philippines and became a global phenomenon. Evolving from its initial function of assisting Axie Infinity in recruiting and training players, YGG is now home to more than 1,500 NFT game guilds based in the Philippines. YGG provides players with digital asset management, game scholarships, and community support—becoming the world’s largest NFT gaming guild.

According to Playercounter, more than 40% of Axie Infinity players hail from the Philippines alone. Play-to-earn has proven to provide meaningful income to users, effectively alleviating economic pressure caused by the pandemic for many users.

This model of massive user acquisition to drive ecosystem growth is a unique characteristic of blockchain development in the Philippines. We anticipate that with the mass inflow of capital and users, there will be a corresponding entrepreneurial response that will lead to the creation of new and innovative applications in the Philippines. We have seen this trend emerge with projects like NFT marketplace Vention and gaming guild management and data platform BlockchainSpace.

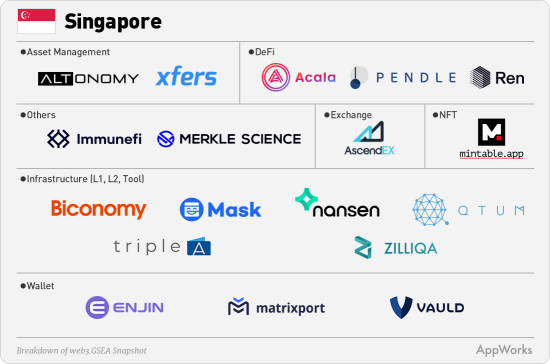

Singapore: Leveraging the Strength of Asia’s Financial Center

Singapore has always been known as Asia’s financial center, building off the government’s proactive policies over the past several decades. A similar trajectory is also taking shape in the country’s blockchain development. The Monetary Authority of Singapore (MAS) is the leading regulatory body overseeing cryptoassets, and has long demonstrated a relatively open and friendly stance on the development of blockchain and cryptoassets within the city-state.

As early as 2017, MAS issued “A Guide to Digital Token Offering” which established the Singapore government’s policy framework for ICOs, issuers and related platforms, under the purview of the Securities and Futures Act (SFA). In January 2021, the “Payment Service Act” (PSA) was launched, regulating all cryptocurrencies, exchanges, and digital payment services in Singapore.

As a result, there has been an emergence of several new blockchain-related applications. For example, Biconomy, which builds transaction infrastructure for blockchain applications and optimizes cross-chain transaction experience; Xfers, a developer of financial electronic payments; and Vauld, a service provider covering cryptocurrency transactions, lending, and wallets. In the future, we expect more projects coming out of Singapore in cryptocurrency-related asset securitization, license compliance, and international exchanges.

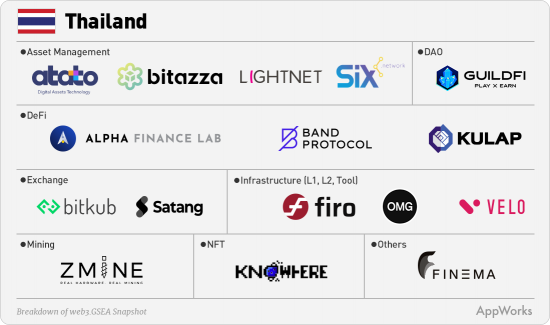

Thailand: From Late Mover to Frontrunner

While Thailand’s blockchain ecosystem can be considered quite early, 2021 marked an acceleration point with several milestones. In November, Thailand’s first blockchain unicorn was born as crypto exchange Bitkub sold a 51% stake worth US$535 million to Siam Commercial Bank. Paired together with logistics provider Flash Express’s newly minted billion-dollar valuation, Thailand welcomed its first unicorns of the internet and Web3 era respectively within a five-month period.

Bitkub’s success is galvanizing the Thai blockchain ecosystem, demonstrating that Thailand can develop scalable blockchain infrastructure. Bitkub alumni and seasoned Web2 entrepreneurs are diving into Thailand’s blockchain space, just as we’ve witnessed in other markets.

In fact, we can already see the emergence of more mature and advanced Web3 applications. For example, the emergence of cross-chain data oracle platform Band Protocol and metaverse gaming guild GuildFi show the level of innovation and reiteration happening in the market. We believe that in the near future, we will see more projects in the NFT space, building off Bangkok’s rich fashion and design industry and the country’s active NFT artist community.

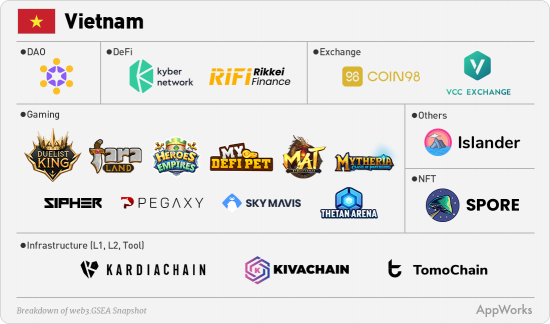

Vietnam: The Axie Infinity Effect

When it comes to Vietnam, the most well-known player is Sky Mavis, the developer behind the killer NFT-based game Axie Infinity. According to CryptoSlam statistics, since its launch in 2018, the total amount of NFT transactions on Axie Infinity reached more than US$3.7 billion, with more than two million daily active users, culminating in Sky Mavis’s recently completed US$152 million Series B round of financing.

The impact of Sky Mavis’s success on Vietnam can be observed from two perspectives. First, it is driving the growth of Vietnam’s local NFT gaming ecosystem and attracting international capital to accelerate development and adoption. For example, in October, Sipher raised US$6.8 million in seed financing from major global investors. In addition, there’s been a surge in casual and semi-casual GameFi projects coming out of the woodwork including My DeFi Pet, Mytheria, Thetan Arena, and Faraland.

Second, Vietnamese users have demonstrated high levels of acceptance for blockchain and cryptoassets. According to the 2021 Global Crypto Adoption Index survey conducted by Chainalysis, Vietnam ranked first globally in terms of overall adoption. Among three indicators, on-chain value received, on-chain retail value received, and P2P exchange trade volume, Vietnam ranked in the top five in the world. We anticipate that new applications in DeFi, wallets, and asset management like we see with Kyber Network’s Liquidity Hub will highlight the next wave of blockchain innovation in Vietnam.

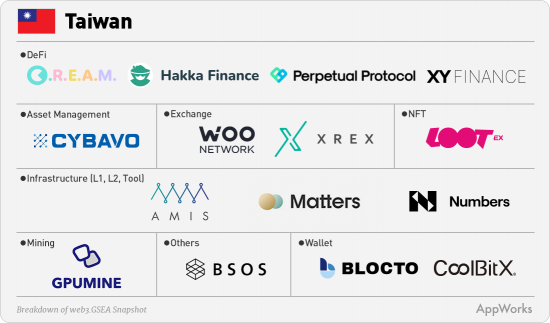

Taiwan: A Huge Digital Market Driven by Engineering Talent

Compared with other markets in the GSEA region, Taiwan has two notable characteristics and advantages in blockchain development. First, Taiwan is home to a massive digital gaming and entertainment market. To illustrate this market size, according to App Annie, in 2020, Taiwanese consumers spent US$2.44 billion in the App Store, equal to total spending from Indonesia, Thailand, Vietnam, the Philippines, and Malaysia combined. Second, Taiwan has accumulated a wealth of engineering talent across manufacturing, software, and hardware integration. This talent pool has formed the core of Taiwan’s blockchain industry.

In 2021, Taiwan also joined the global NFT wave with early-stage activity. Leveraging the island’s fertile digital gaming and entertainment market, Taiwanese founders are adopting NFTs to create products, services, and new business models. Musicians, artists, game publishers, and influencers have embraced NFTs to build public awareness and tap into this new digital format of ownership, demonstrating immense promise for large-scale commercial adoption of NFTs.

Since the advent of Ethereum, Taiwan’s local engineers have continued to explore the frontiers of blockchain development, becoming a key driving force in the crypto world. Taiwan is home to several notable projects led by seasoned teams, including Perpetual Protocol, which provides Virtual Automated Market Maker (vAMM) to implement perpetual contract solutions; smart contract wallet Blocto has become the go-to wallet for Flow—with more than 80% of Flow users trusting Blocto for Flow Token pledges. In cross-chain applications, Blocto also supports Ethereum, BSC, Solana, Avalanche (c-chain), and Polygon, among other mainstream public chains.

Bright Days Ahead

Just a few years ago, you’d be hard pressed to find the words web3, blockchain, DeFi, or NFTs uttered anywhere outside of niche crypto spheres in this part of the world. Now, sentiment from founders and investors across the region have evidently shifted from “why web3?” to “how do I get a piece of it?”—largely in this past year alone.

Taiwan is at the forefront from a technical perspective, with an unparalleled engineering pool in terms of cost and performance; Indonesia is emerging as massive market for web3 consumers, now with crypto traders outnumbering stock traders by severalfold; Philippines is in a close second, with everyday users showing an uncanny demand for GameFi to make ends meet; Thailand’s historically nascent ecosystem is expected to garner significantly more attention now with their first crypto unicorn; Vietnam, given Axie’s success, is quickly distinguishing itself as a the world’s NFT gaming hub; and lastly, Singapore’s position as the region’s financial and management hub will likely extend into the web3 era.

Any doubts of whether or not web3 is here to stay were certainly eroded by the massive strides that the regional ecosystem has taken in 2021. Looking forward, the development and adoption of web3 is looking especially bright. Although crypto markets will likely ebb and flow in the coming months and years, with the occasional bears and dips, many stakeholders across the value chain have already gotten taste, and will likely only want more.

The 2021 Greater Southeast Asia Blockchain Ecosystem Map is authored by AppWorks. For inquiries, please write to [email protected]. For this survey, thanks for several friends’ assistance: Peter Ing (Co-Founder of BlockchainSpace), Leo Pham (Manager of Access Ventures), Hung Nguyen (CEO of Spores), Tri Pham (CEO of Kardiachain), Ben Minh Le (CRO of M3TA), Rémy Perettieny (CEO of Reminiscense), TN Lee (Co-Founder of Pendle Finance), Lawrence Samantha (Founder of NOBI), and Eagle Su (Marketing Specialist of Zombit)

【If you are a founder working on a startup in SEA, or working with AI, Blockchain, and NFT, apply to AppWorks Accelerator to join the largest founder community in Greater Southeast Asia.】

事實上,我們還有更大方向的討論,就是我們要選擇 To B (面對企業用戶的服務) 或 To C (面對個人用戶的服務) 的商業模式。我們覺得 To B 的模式比較不容易 Scale up,一次做一個案子,也許可以賺到一些錢,初期現金流可能比較穩,但如果要做兩倍大的案子,可能團隊規模也需要等比放大到兩倍。另一方面,To B 要配合客戶的需求,對我們來說,也比較不自由、不那麼有趣。

若是走 To C 的模式,如果我們可以做出一個夠好、我們自己也喜歡的產品或服務,用戶數的成長空間將非常寬闊,真的可以看到因此為人們帶來更大的影響力。當時,已經有不少高效能的公鏈出來,各種交易所更是比比皆是,反而比較大的問題在使用者體驗,因此選擇 To C 模式、切入錢包這個題目,這倒是有很高的共識。

Edwin: 從另外一個面向來說,To B 比較像是企業客戶出考題,跟對方聊完,就會知道他要與不要什麼,我們需要解決哪些問題。To C 則完全相反,就是要從市場反應中快速調整,逐漸做出現在的樣子,我們在過程中也做過一些市場調查,但做出來的成果,就是會有一些人喜歡、一些人不喜歡,比較像是我們自己要去發掘問題,出考題給自己去解決。

但也正因為這樣,我自己覺得做 To C 有一種比較浪漫的感覺,尤其是在區塊鏈產業。就有一種眾志成城的感覺,看著用戶數量慢慢累積起來的過程,很有趣也很有成就感。

David is an Associate mainly focused on investments. He previously lived in the US, but was drawn to the Greater Southeast Asia region by the growth opportunities and the wonderful people here. He spent the first five years of his career as a consultant at IBM, where he became intimately familiar with the enterprise software and services needs of Fortune 500 companies. Later, he focused on building predictive models and solving optimization problems for large companies, and gained an appreciation for the role of data and algorithms in our lives. He joined AppWorks in 2020 after receiving his MBA from Columbia Business School, and also has a B.S. in Mathematics from the Ohio State University. In his free time, he tries to stay active and is always looking for opportunities to hike or trek, often seeking the trail less traveled.

In “The Market for Lemons,” George Akerlof described frustrated sellers of high-quality used cars not fetching a fair price because the prospective buyers were unable to distinguish between high-quality used cars and low-quality ones (known as “lemons”), that on the surface looked identical. Sellers could only find takers at a discounted price taking into account the possibility they were buying a lemon. Those who have experienced swift price depreciation upon driving a new car off the lot know this well intuitively. Eventually, sellers of high-quality used cars leave the market, as they cannot be fairly compensated due to the market’s inability to appraise their vehicles fairly.

A new study suggests that the same applies broadly to entrepreneurs. It is impossible for companies to 100% accurately appraise the capability of job applicants and current employees. Hiring managers tend to assess talent based on traditional credentials, such as educational background and work experience at prestigious schools and companies. And managers tend to assess current employees through a combination of perceived signals, personal bias, and company politics. Those who may be highly capable but lack traditional credentials or particular signals sought by senior management (akin to the frustrated sellers of high-quality used cars) withdraw from the labor market and ultimately choose entrepreneurship instead, a path to earnings not constrained by uninformed buyers of labor on the market.

Going from unhireable to startup founder may sound fanciful, but there are some high profile examples. Brian Acton’s capabilities were not accurately assessed by Facebook and Twitter, where he failed to pass the interviews in the summer of 2009. By November, he joined San Jose State University dropout Jan Koum in starting WhatsApp, which the duo later sold to Facebook for US$19 billion.

Many immigrant entrepreneurs face the same choice when they arrive in a new country that does not recognize their foreign degrees or accomplishments. They can either work low-level jobs not requiring any credentials, or they can start small businesses and capture more of the value of their talents.

More precisely, the study finds that entrepreneurs tend to be those whose talents are better than the credentials and abilities readily observed by outsiders. When we choose to go work for someone, the company retains our productivity minus our wage, which is based on the company’s assessment of our “market value”, or the cost of replacing us with another worker who shares similar backgrounds and experiences. Those who feel that the gap between their productivity and their market wage is too wide can take the entrepreneurial plunge and, if everything works out, capture the entire value of their productivity.

A separate but related finding was that “entrepreneurs have higher cognitive ability than employees with comparable education.” If those with comparable educations exhibit comparable signals and end up at similar jobs and companies, it suggests that many entrepreneurs decide they’re out of place, “cognitively” speaking, even when surrounded by similarly credentialed peers at their job. Their boss might see them as just another employee, but the would-be entrepreneur believes this is wrong, and that they should be several titles up, running entire departments or even the whole company. They can’t fathom how the ship is being run, and since the company can’t evaluate their true value and compensate accordingly with much higher responsibilities and pay, they decide to run their own ship.

On the flip side, those underperforming yet well-credentialed workers that exhibit positive observable signals can’t believe they’re getting paid so much to add so little value. They would thrive in a large corporation that is blind or apathetic to the fact that the worker is capturing the gap between their high wage and their scant contributions. These lucky workers would find no incentive to pursue entrepreneurship, where the market would discover their true value.

Intuitively, I think this makes sense and matches what I have observed at AppWorks. A lot of great founders have elite degrees and prestigious work experience, but they look around at their workplace and think: “This is a great gig but I’m capable of so much more in this life.” Other great founders went to average schools or were late bloomers stuck at middling companies and didn’t have any luck applying to elite companies and jobs, perhaps due to their lack of pedigree. They couldn’t bear delaying greatness any longer and took matters into their own hands.

I asked a couple of our portfolio companies’ founders for their take, including Wayne Huang, co-founder and CEO of Taiwan-based XREX (AW#17), a neo-fintech that solves dollar shortage issues for cross-border merchants in emerging economies that recently announced a US$17 million financing.

“I can quite relate to this,” the second-time founder said. “It was just obvious to me that I wouldn’t be happy with the employment opportunities that I had when I graduated. I was just not going to be happy. That part I understood very well.”

Indah Maryani, co-founder of InfraDigital, a company digitizing Indonesian schools’ data and billing, had frustrations as an employee at a previous startup. “You’re not an owner or an investor. You don’t own the vision; others are driving it. We said it should be done another way, but it was hard to convince the others. So my co-founder and I said, let’s create another company and build it ourselves,” she says. So they did.

Of course, this is an academic study. It would be presumptuous to suggest that an entrepreneur’s or employee’s motivations are purely financial (though the study did control for several correlates of entrepreneurial choice, such as worker wealth, risk-taking, locus of control, and other demographic features). I would also argue that the capability to add economic value is not the same as the capability to add entrepreneurial value.

But it does shed light on some of the common thoughts and fundamental drivers of entrepreneurs. “I’m more capable than this.” “I feel out of place among my coworkers.” “Is this all the impact I’m going to make in this life?” “My work is useless or misguided, and I can’t believe my boss can’t see it.” “Why am I working so hard for these wages?” “I’m not getting the respect I deserve—let me prove that I’m way more capable than this.”

After simmering in these types of thoughts, entrepreneurs of all colors make the jump, despite how scary, lonely, and risky the journey is. They move toward the entrepreneurial abyss, despite skepticism by their peers, doubts by observers, and mockery by salaried workers, all things that exist in today’s society which values so much name brands, stability, and validation by others. Despite risking being viewed as overconfident, egotistical, or doing it because they can’t find a good job, they set out on the journey anyway. They have a special drive that enables them to do this, and perhaps part of that drive for some entrepreneurs is the information asymmetry between actual talent and perceived talent.

I suppose you could say we’re lucky that this information asymmetry exists. Without it, some founders would instead find high-level jobs, having his or her hands on the wheel while adding great value at great companies, getting richly compensated, and perhaps even being able to spin their divisions off while having significant equity ownership. Instead, they embark on the difficult road of entrepreneurship, and in the process create massive value that only a startup founder could possibly create — more value than they ever could have imagined. Making lemonade out of lemons.

【If you are a founder working on a startup in SEA, or working with AI, Blockchain, and NFT, apply to AppWorks Accelerator to join the largest founder community in Greater Southeast Asia.】

Jack is an Analyst covering AppWorks Accelerator. Before joining the team, he was a co-founder and early team member at two InsurTech startups, where he developed a passion in user experience and product development. Previous to his startup journey he worked as a commercial property underwriter at Chubb Insurance in New Zealand. Jack graduated with a Bachelor of Music from Waikato University where he studied classical piano. He loves to cook, read and is a practicing stoic.

During the first half of 2021, public interest in blockchain reached an all-time high. Towards the end of last year, we saw an upswing in the number of organizations and enterprises buying and holding cryptocurrencies, causing the price of Bitcoin to cross US$60,000 for the very first time in March. Talk of crypto quickly made its way into dinner table conversations, and it seemed as if everybody on the block was eager to dive into the world of blockchain.

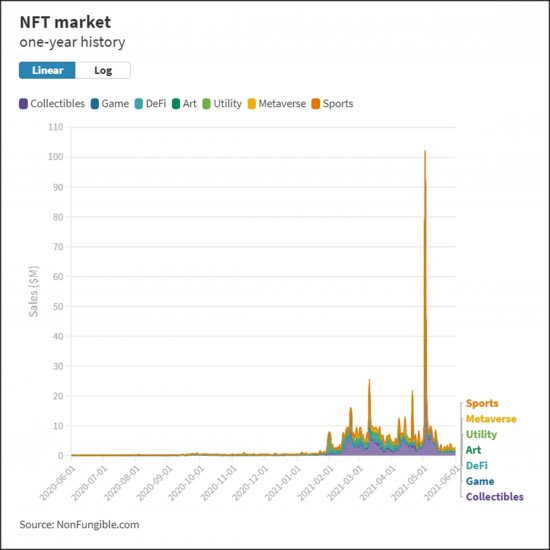

For those that have been in crypto for a while, this bull run finally let them exit many of their alt-coin investments from the 2017 ICO wave, as the wider market price sentiment rallied alongside the mainstream coins to reach an all time high. The other worthwhile trend over the past six months has been the mainstream adoption of NFTs (non-fungible tokens), a technology that provides true ownership capabilities and authenticity over digital assets. We saw hoards of multinational brands, intellectual property owners, celebrities, and individual creators quickly embrace this new technology and flock to various platforms to either buy NFTs or mint some of their own.

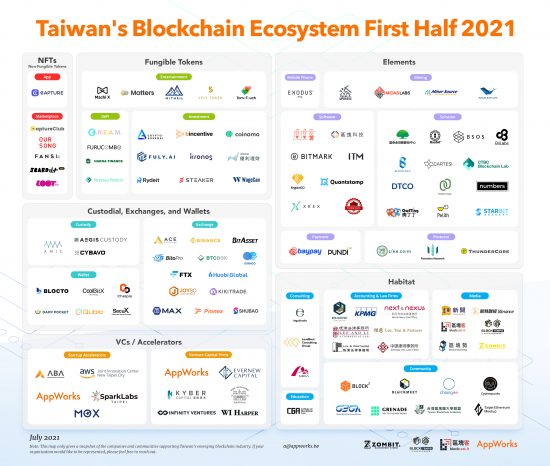

It’s certainly been an exciting ride since AppWorks Accelerator started publishing Taiwan’s Blockchain Ecosystem Map two years ago. In line with previous editions, we’ve observed several notable trends that have defined the blockchain industry this past half year.

1. Branded drops accelerated end-user adoption of NFTs

The NFT standard was formulated in 2017, so why did it only catch on this past year? It really came down to two key driving forces. First, mainstream brands and IPs started employing NFTs as a vehicle to interact with their fans, such as the NBA through NBA Topshot, Taco Bell, and even the band Kings of Leon. By creating a virtual experience through NFTs, brands were able to engage and create a unique bond with their loyal fans despite physical restrictions under COVID-19, allowing them to also generate alternative revenue streams from the sales of NFTs.

Second, NFTs are becoming an alternative asset class for yield-driven crypto holders and investors. During the ICO era in 2017, most developers and investors were either busy issuing coins or trying to find the next cryptocurrency with hundred-fold growth potential; it wasn’t long until this model became monotonous and out of fashion. Fast forward to 2021, decentralized finance (DeFi) hit a US$100B market cap and drove crypto prices to all-time highs. As NFTs started emerging, crypto holders were naturally drawn to their consumer appeal and accretive potential, propelling NFTs into the limelight for mass adoption. Much of this adoption is supported by advancements in the underlying infrastructure, including a growing ecosystem of protocols, marketplaces, games, developers, creators, and of course, buyers.

Evidently, a lot of moving parts have come together in the last few years to catapult NFTs into stardom. In Taiwan, the NFT landscape has also evolved significantly compared to the second half of 2020. For example, Lootex, an alumnus of AW#20, and Oursong, a subsidiary of KKBox, both established NFT products long before the recent bull run. All the effort they put in during previous cycles are now bearing fruit, with both companies receiving an influx of new partnerships and commercial opportunities. During this time, we also saw a proliferation of new NFT players, such as JCard and Fansi, effectively creating a diverse selection of platforms for creators to choose from.

With Beeple’s First 5000 Days selling for US$69 million, celebrity engagement, and primetime media including even SNL releasing NFT coverage, all the major signs of a bubble were there. And surely enough, monthly transaction volume experienced a significant decline of 90% shortly after its record high in May. Nevertheless, as witnessed with previous blockchain hype cycles, where there is money, there will be talent, and where there is talent, there will be development. Ultimately, NFTs are still in the early innings, and while collectibles have served as the primary use case so far, this new technology will eventually extend across any product, service, or application that needs to use a digital ID.

2. Taiwan’s regulation catching up to the world

Up to recently in Taiwan, the laws and regulations related to cryptocurrency have been very vague. And for those trying to stay compliant, they could only follow the existing but outdated mandate, or hope for the best by following foreign regulations. This was changed in April this year, as the Executive Yuan aligned their stance with the rest of the world by implementing strict AML/KYC requirements when dealing with cryptocurrencies.

Existing players like MaiCoin—the primary fiat-to-crypto exchange in Taiwan—faced minimal impact as stern KYC controls were already in place. However, teams working on DeFi, lending, and investing may face greater obstacles, as it is challenging to design a user experience in a decentralized manner that complies with regulations while still adhering to the spirit of decentralization—a faux pas that many blockchain founders and evangelists are becoming increasingly critical of. Going forward, we expect decision makers to implement more comprehensive and tailored regulations for DeFi to prevent bad actors from gaming the system and taking advantage of everyday consumers; this will ultimately encourage more users and wider adoption, benefitting the ecosystem as a whole.

3. Influx of funding and talent set to accelerate development

With the price of bitcoin hitting an all-time high in H1 2021, investors around the world are taking note of the industry’s activities. For example, in May this year, DApp Pocket (AW#19) announced that they had been acquired by Turn Capital, a family office run by 17LIVE co-founder Joseph Phua. It also merged its two products, DApp Pocket & Cappuu, into Coinomo, with the aim of bringing crypto to mainstream users in Southeast Asia.

At the same time, another blockchain wallet developer in Taiwan Portto (AW#19, AppWorks is an investor), whose product Blocto serves as one of the earliest wallets supporting Flow and the largest delegated node by user count to stake Flow tokens, recently announced the completion of a US$8.8 million fundraising round. Primary investors include top blockchain VCs from Silicon Valley and Taiwan, as well as participation from a notable crypto exchange, public chain foundations, NBA players, and well-known American entrepreneurs, among others.

Despite a significant price correction in cryptocurrencies since May, the momentum that has been brewing over the past six months will likely pay off in the second half of the year, whether through DeFi, NFT, or blockchain applications at both the consumer and enterprise level. We’ve also started to observe more international companies such as Animoca Brands (AppWorks is an investor) enter Taiwan to recruit top-tier blockchain talent, which is expected to further accelerate the development of the country’s blockchain ecosystem.

Taiwan’s Blockchain Ecosystem Map First Half 2021 is created by AppWorks, Co-produced by Blockchain Media – Blockcast (AW#14), BlockTempo (AW#16), Zombit (AW#21). This map is updated every six months, if you have any comments or suggestions don’t hesitate to contact us at [email protected].

【If you are a founder working on a startup in SEA, or working with AI, Blockchain, and NFT, apply to AppWorks Accelerator to join the largest founder community in Greater Southeast Asia.】