DeFi already has Aave. So the first question anyone may ask is why build another lending protocol.

Yet if one digs deeper, they will realize capital fragmentation still creates a huge structural inefficiency in DeFi today. The same dollar of collateral that backs a loan on Aave cannot also be an LP position on Uniswap. Aave, Compound, and Uniswap each wall their liquidity off from one another, so capital sits in one silo doing one job. Therefore, the world does not need another lending protocol, but we can all benefit from solving this structural inefficiency.

That’s why the world needs Fluid: it collapses those walls. The same collateral that secures a loan can finally also provide trading liquidity at the same time, and it shows up the cleanest measure of capital efficiency, revenue per dollar of TVL, where Fluid runs about 0.43% in 26Q1, the highest of any lending protocol.

But the number is not why we invested. What we care more is the team who can break the constraint while others just live with that.

Samyak Jain: The math geek who rebuilt everything from first principles

Samyak and his older brother Sowmay grew up in Kota, India’s academic-pressure capital. Samyak watched The Social Network in ninth grade and decided he wanted to start a company. He was a math prodigy and a competitive chess player. Sowmay started trading Indian stocks in high school and wrote his own apps to track them, and Samyak joined in to write the code. That was their first project together, and it ran straight into the walls of traditional finance, where your age, a missing license, or a lack of capital can simply lock you out.

On his first day of college, Samyak told his parents he would drop out the moment he found an idea worth it. The idea showed up fast. In August 2018 the brothers entered the ETHIndia hackathon, built a tool on top of MakerDAO, and won. The takeaway stuck with him: two college students could write code that managed millions of dollars, and no one could stop them. They were crypto-native from the start, with a MetaMask wallet before a bank account. In 2019 Pantera and Naval backed them with $2.4M, Samyak dropped out, and they went all in on Instadapp. It became DeFi’s leading middleware and peaked at around $12B in TVL.

Then came the moment that decided everything. In 2022, when LUNA collapsed and stETH lost its peg, Instadapp’s Lite strategy came close to roughly $1B in liquidations, and the team scrambled through emergency loans to survive. Samyak’s own summary is that those three days taught him three years’ worth of risk lessons. The most important one was simple and uncomfortable: middleware sits on top of other people’s protocols, and you cannot fix a broken foundation from the top. Most founders sitting on a $12B protocol would have kept shipping features. Samyak did the opposite. He stopped iterating on Instadapp and spent close to a year and a half rebuilding lending from the ground up, around one question: what would a bank look like if you built it from zero on-chain?

Early 2026 put both the founder and the architecture through two real tests. In March, an attacker exploited a partner protocol, Resolv, and pushed about $80M of unbacked tokens into Fluid. Two things saved it. Fluid’s automated risk limits capped how much damage that bad collateral could do before any human reacted. And within about half a day, the team had sized the loss, lined up interest-free emergency loans from partners like Cyberfund and Jupiter, and publicly guaranteed user funds, which stopped a panic before it could start.

The second test was system-wide. In April, a hack at Kelp set off a bank run across DeFi: everyone rushed to pull ETH out of lending markets at once, Aave’s ETH was fully borrowed out, and the cost of borrowing ETH spiked everywhere. Within hours, Fluid shipped a tool (its aWETH Redemption Protocol) that let lenders who were stuck in Aave get their ETH out, and in the process reduced Fluid’s own exposure at the same time. Fluid came out of the crisis looking like the lender of last resort.

Fluid could have simply waited for Resolv to resolve its own exploit. Instead the team acted first, taking measure after measure to make sure user assets were protected. That perseverance, and the instinct to put user funds ahead of everything else, is what impresses us most. This is the kind of founders we at AppWorks are proud to back: those that are willing to rebuild from zero. On top of that, across both crises, what stood out was the speed and capability with which the Fluid team handled them.

Beyond the design: how Fluid grows

We won’t rehearse the mechanics here. The design is genuinely clever, with three pieces doing the work (Smart Collateral, Smart Debt, and the liquidation engine), and Cyberfund has already written the clearest explanation of how they fit together in its two-partDemystifying Fluid series.

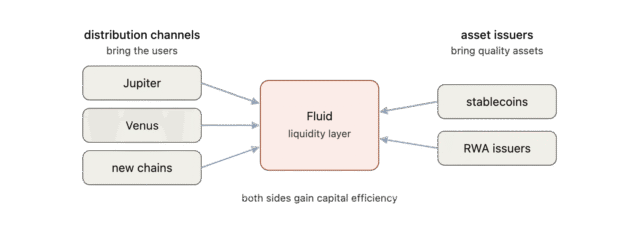

What we like just as much as the design is the go-to-market. Fluid runs its own protocol and is still building its own community, but its biggest growth lever is distribution: it takes the same engine and plugs it into channels that already have millions of users, instead of trying to win every user directly.

Jupiter is the clearest example. It is Solana’s largest trading aggregator, so Fluid provides the lending engine, Jupiter brings the users, and together they launched Jupiter Lend with the economics split roughly fifty-fifty. The deal closed fast because the founders already trusted each other. On BNB, Venus, the chain’s largest lending protocol, now runs on Fluid through Venus Flux. And institutional curators are starting to arrive: Bitwise runs an Ethena market on the Fluid-powered Jupiter Lend, the first institutional-grade curator on the system.

It is worth being precise about where the moat comes from. The obvious part is lock-in: once Fluid is the lending engine underneath a partner like Jupiter or Venus, ripping it out is so costly that almost nobody does, and Fluid gets there without paying for users through token emissions, the most expensive game in DeFi. But the deeper moat is less glamorous. Running a lending book well is genuinely hard operational work. Every collateral type needs its risk parameters set and watched, liquidations have to stay ahead of fast-moving markets, and the whole book needs constant risk management. Most teams do not want to touch any of that, which is exactly why being the team that does it well, on everyone else’s behalf, is so hard to dislodge. It also just makes economic sense: powering a partner earns Fluid far more than launching yet another vanilla lending protocol on its own would, so the partnership pays off for both sides.

That points to the bigger picture: Fluid is really a two-sided platform. On one side are the distribution channels we just described, the apps and chains that want a lending and trading engine without building one themselves. On the other side are the projects that need liquidity, like stablecoin and real-world-asset issuers, who can use Fluid’s pools to bootstrap a market far more cheaply than hiring a traditional market maker. When the reUSD stablecoin launched on Fluid, its TVL and trading volume jumped in a single day, and it has since spread across multiple chains. Fluid sits in the middle and makes both sides more capital-efficient than they could be on their own.

The thing to understand is that these are not separate product lines. They are one architecture. Fluid is a single liquidity layer that any number of protocols can plug into, where the same capital is reused across spot, perps, FX, and credit. DEX, Perp, and FX are not different businesses, they are the same engine reaching into new asset classes, and each one adds revenue without needing fresh TVL. The north star is to rebuild banking from zero on-chain: to become the engine behind banks and neobanks, to bring real-world assets on-chain, and to make the kind of 95% LTV borrowing that today only billionaires with private bankers can get available to everyone.

—

We’re thrilled to back Samyak and the Fluid team as they rebuild banking from first principles on-chain, turning capital efficiency from a feature into the primitive the next financial system runs on.

And if you are a founder building on-chain banking from first principles, we would love to talk.

專攻 3D 空間感知與邊緣 AI 系統的 LIPS,憑藉深厚的底層技術,已成功獨家供應德國 BMW 工廠自主移動機器人(AMR)的 3D 視覺導航大腦。此外,LIPS 更為新北市打造了全台最大規模的 7×24 智慧交通數位孿生監控系統,實績橫跨智慧製造與城市基礎設施,展現極高技術壁壘與跨國大廠的商業落地實力。

SixSense 則是專為半導體與電子製造業打造的 AI 平台,能精準辨識產品缺陷並預測設備維護需求。透過先進的電腦視覺模型,全自動檢測並精準分類晶圓上的微觀缺陷,有效取代了耗時的工程師人工複查流程,顯著加速產線週期,並為全球半導體晶圓廠預防因良率損失造成的巨大經濟折耗。

打破跨境文化與數據壁壘:韓國優質新創強勢登陸台灣

本屆 Demo Day 的另一大核心亮點,在於成熟營收能力的韓國新創,開始選擇台灣作為跨國擴張的樞紐。

NOTAG KOREA 由深耕跨境貿易運營逾十年的創辦人 Aiden 創立 。由於跨國電商平台碎片化、物流體系繁雜且跨境數據格式極不標準,自動化營運難度極高,所以目前成功進軍東南亞與台灣的韓國時尚與美妝品牌不到 0.3%。NOTAG KOREA 獨創 AI 自主運營引擎,一鍵打通多國銷售通路與物流鏈 ,目前已成功將 Emis、HDEX、Covernat 等 204 個韓國知名品牌引進海外 105 個銷售通路,創造高達 400 萬美元的跨境年營收 。

韓國的 Deep Tech 代表 Clika,推出邊緣運算 (Edge AI) 的自動化模型壓縮平台。針對企業在工廠與裝置端部署 AI 時,面臨晶片太貴、太耗能的痛點,Clika 的核心技術能在不犧牲精準度的前提下,大幅壓縮 AI 模型體積,使其能流暢運行於低算力的微型晶片中,直接降低企業導入 AI 的硬體門檻與成本。

Notifly 創辦團隊來自 Airbnb、Coupang、Toss 與 Naver 等大廠,深諳亞洲通訊服務底層架構 。他們打造出 Kakao 原生且完美適配 Line 生態的 AI 企業訊息自動化平台,已協助包含 CJ Logistics在內的 143 家大型企業客戶自動化經營用戶旅程,月處理訊息量破億,在年化營收(ARR)突破百萬美元大關的同時,寫下 96% 的客戶留存率 。

Krush 是專為全球泛亞洲族群打造的跨國社交網路與實體社交俱樂部。團隊打破傳統交友軟體的單向框架,透過 AI 人臉防偽驗證與實體活動媒合,寫下 57% 的次週留存率,預估年化營收將達 200 萬美元。

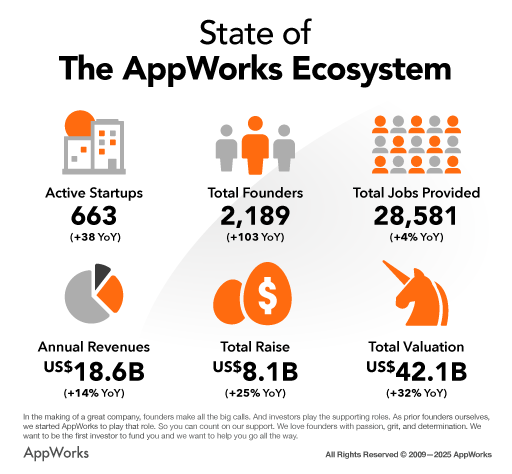

SINGAPORE, 9 June 2026 — AppWorks Accelerator has officially introduced its latest batch, AW#32, a cohort that has marked the leading startup incubation program’s deliberate shift toward deep tech through its specialized Requests for Startups (RFS) recruiting process – Manufacturing AI, Defense Tech, and On-Chain Banking specifically for this batch. Operating an equity-and-fee-free program, AppWorks continues to grow Asia’s largest startup network, which now encompasses 663 active companies and over 2,189 founders collectively generating USD 18.6 billion in annual revenues.

This cohort reflects a powerful evolution within the regional tech landscape: the convergence of critical hardware infrastructure with advanced software, alongside a highly mature wave of South Korean startups utilizing regional networks to execute cross-border expansion strategies..

As a long-term investor and strategic partner of AppWorks funds, K.S. Pua, Founder, Chairman, and CEO of Phison, joined the event to mentor and exchange insights with the next generation of founders.

Reflecting on his own journey, he shared: “As an engineer by training, I co-founded Phison with just a $1M seed fund – nothing more. We bootstrapped our way to profitability within our first year, turning Phison into the publicly traded memory solutions powerhouse it is today. As a founder, your survival depends on agility. In this AI era, Phison has pivoted to deliver energy-efficient, high-performance, and secure computing storage solutions, capturing strong market demand. For today’s founders, this is a golden age for AI entrepreneurship, but this window of opportunity will only last for the next 3 to 5 years – act now before it’s too late.”

To further accelerate this momentum, Phison is currently planning to launch a Corporate Venture Capital (CVC) arm to back startups and drive future growth.

Revolutionizing the Factory Floor: The Rise of Manufacturing AI

By tying into Taiwan’s global hardware manufacturing and supply chain ecosystem, AppWorks has positioned itself as the premier launchpad for builders deploying production-ready AI within complex industrial environments.

Leading this charge is Innowave Tech, an enterprise autonomous factory platform spearheaded by founder Jinsong, who brings over 25 years of semiconductor fab leadership experience from GlobalFoundries. Innowave Tech addresses critical industrial labor shortages and operational bottlenecks by replacing slow human defect inspection with a proprietary foundation model capable of millisecond-level, closed-loop autonomous decision-making. Deployed globally across semiconductor fabs, the system has successfully automated defect processes while driving measurable enhancements of over 10% in Overall Equipment Effectiveness (OEE).

Complementing this industrial revolution is LIPS, which delivers a comprehensive “Digital Eye” spatial compute infrastructure tailored for smart factories and smart cities, deploying high-precision 3D vision systems that have already secured tier-one validation from global automotive manufacturing giants such as BMW.

The New Cross-Border Pipeline: South Korean Startups Scaling Internationally

A standout paradigm shift in Batch #32 is the high concentration of mature South Korean ventures scaling across Greater Southeast Asia and Taiwan.

Leading this narrative is NOTAG KOREA, a commerce and logistics automation AI engine founded by Aiden, an entrepreneur with over a decade of experience in e-commerce-based trade and distribution. The platform automates logistics and distribution, overcoming the high entry barriers that prevent 99.7% of Korean brands from expanding into SEA. Through real-time data analysis and sales forecasting, their engine cuts inventory costs and expansion friction. To date, NOTAG KOREA scales 204 brands across 105 hubs, capturing USD 4 million in cumulative revenue.

Refundy introduces an automated refund optimization system for global B2B marketplaces when platform prices fluctuate, empowering merchants across 55 countries to recapture margins while driving strong, profitable monthly recurring revenue (MRR) of nearly USD 150,000.

Meanwhile, Krush breaks the mold of standard matchmaking apps by engineering a transnational social network and “social club” for global Asians, capitalizing on cross-border interaction to achieve a 57% Day-7 retention rate — proving that people are looking for more than matches; they are looking for a sense of belonging.

Driving Global Innovation Across Deep Tech, Web3, and Enterprise Software

The remaining cohorts of the Singapore showcase highlight highly specialized applications tackling complex multi-market operational workflows.

In the deep tech and dual-use space, unmanned vehicle architect Juan Herrero founded Hyarks to deploy autonomous fleets of marine vessels that source real-time oceanic data. This marketplace solution eliminates the USD 1.9 billion in searching waste endured by commercial fishing fleets while simultaneously tapping into a USD 500 million defense opportunity in APAC.

On the financial security front, Novo AI enables health insurers to detect fraud, abuse and hidden claims leakage within complex, unstructured medical and billing documents. Founded by former Google leaders, the company works with enterprise insurers like Tokio Marine and April Group to improve loss ratios, automate workflows and drive smarter decisions across 4 continents.

Infrastructure capabilities are further advanced by Pathors, which supplies a hyper-low-latency enterprise Voice AI engine delivering response times under one second to optimize call-center efficiencies.

Catering to the building sector, Rosary Labs deploys AI agents for Architecture, Engineering, and Construction (AEC) industry, converting drawings from PDF to CAD to BIM, and automating BIM review and bill of quantity generation, reducing costly human error, ensuring compliance for public sectors and increasing tender success rate for top developers.

In market research, Decisions Lab shortens standard corporate go-to-market lifecycles through an AI buyer simulation engine that role-plays target consumer personas with high accuracy.

Last but not least, Shieldbase, founded by Diego Rojas, it’s an AI operating system for the enterprise with strong focus on governance and security

The presentation of these 11 standout teams at Demo Day #32 marks just the beginning of their cross-border growth journeys. By equipping this batch with rigorous pitch reframing, tailored corporate matchmaking, and localized landing infrastructure, AppWorks continues to solidify its role as the ultimate launchpad for deep technical moats and cross-border expansion in Greater Southeast Asia.

Alyssa Chen, Principal at AppWorks, noted: “AI is transitioning from a digital efficiency tool into a core operational necessity for frontline industries. In our AW#32 batch, founders are moving far beyond pure-software applications to embed AI directly into manufacturing and defense, sectors hardest hit by labor deficits. This industrial push inherently anchors their technology in Taiwan’s global hardware infrastructure, creating an unassailable tech moat that is now drawing mature Korean startups to actively scale into our GSEA platform. At AppWorks, we are actively enabling this next generation of pan-Asian winners to orchestrate cross-border resources and execute deep, real-world localization.”

About AppWorks

Founded in 2009, AppWorks is one of Asia’s leading startup accelerators and venture capital firms, supporting over 663 active startups and 2,189 founders. Its equity-and-fee-free accelerator program nurtures founders at every stage, backed by strong regional networks and deep alumni engagement. By focusing on frontier AI and specialized Requests for Startups (RFS) verticals, AppWorks positions itself at the forefront of the region’s digital transformation, providing founders with institutional capital, mentorship, and a vibrant community. For more information, visit appworks.tw.

AppWorks Demo Day #32 Singapore Pitching Teams

Innowave Tech (SG): An enterprise autonomous factory platform powered by a proprietary industrial foundation model enabling millisecond-level, closed-loop defect detection and operational decisions.

NOTAG KOREA (KR): An AI-driven cross-border operations engine that unifies multi-country e-commerce channels and logistics for globalizing Korean fashion and beauty brands.

Refundy (KR): An automated B2B marketplace refund optimization platform that helps international merchants automatically recapture lost margins from platform price fluctuations.

Krush (KR): A transnational social network and physical social club engineered for global Asians utilizing AI anti-fraud verification and high-intent community matching.

LIPS (TW): High-precision 3D vision systems and spatial compute infrastructure designed for industrial automation, smart factories, and automotive manufacturing.

Hyarks (TW): An autonomous marine vessel and drone fleet establishing a global data marketplace to optimize commercial far-sea fishing and regional maritime defense.

Rosary Labs (MY): Specialized AI agents for the Architecture, Engineering, and Construction (AEC) industry that automate manual drafting conversions and quantity estimation workflows.

Pathors (TW): A hyper-low-latency enterprise Voice AI infrastructure engine delivering real-time voice response times under one second to optimize call-center conversion.

Decisions Lab (HK): An AI-powered buyer research simulation engine that role-plays target consumer personas to compress corporate go-to-market validation cycles.

Novo AI (SG): An advanced anomaly detection and risk management model engineered by ex-Googlers to systematically catch paper-heavy leakage and billing abuses for global insurance brands.

Shieldbase (SG): An enterprise-grade data security and privacy infrastructure engine focusing on automated sensitive data de-identification and cross-border compliance.

Founded in 2010 by Jamie Lin, AppWorks Accelerator is a startup community created by founders, for founders.

Every six months, we welcome founders who are building on the edge of what’s possible – those pushing the boundaries of technology and creating what the world has yet to imagine. We equip them with the necessary resources, mentorship, and community to turn bold visions into lasting impact.

We know there are many considerations for founders when applying to an accelerator. That’s why we’ve created an FAQ page to help you decide whether or not AppWorks is the right fit for your startup.

As of Aug 2026, Application for AppWorks #33 is closed, but you can join the waitlist for AppWorks #34You can find important information about the Accelerator experience on our main page.

The FAQs

1. What do I need to know before joining the accelerator? What is AppWorks doing to help founders make the most out of the accelerator?

We understand the unique needs and aspirations for founders, and we’re committed to providing an experience that’s both flexible and deeply supportive:

a. Tailored Events for Founders:

No two founder journeys are alike — whether you’re just getting started, actively scaling, based in Taiwan, or operating from anywhere in the world, we’ve designed a flexible accelerator that blends online and offline experiences. You’ll have access to the resources, mentorship, and connections that best fit your unique path, ensuring that you get what you need, when and where you need it.

b. A Pan-Asia Founder Network:

Beyond flexibility, what truly sets AppWorks apart is our expansive presence across Asia. Our active founder and investor network now spans Taiwan, Singapore, Korea, Japan, Indonesia, Malaysia, Vietnam, the Philippines, and Hong Kong. Wherever you are, you’ll find peers, mentors, and partners who can share local insights, facilitate introductions, and open doors to new cross-border opportunities.

c. Taiwan: Your Strategic Base for Innovation:

Taiwan stands at the intersection of technology, manufacturing, and finance, making it an ideal base for founders building in AI, manufacturing, defense technology, and on-chain banking. Its world-class engineering talent, reliable manufacturing partners, and robust supply chain give startups the speed and stability to develop and scale products efficiently. Combined with an open, innovation-friendly environment and strong digital infrastructure, Taiwan provides everything you need to move from prototype to market with confidence. We encourage founders to join our in-person activities whenever possible. Face-to-face engagement within our community in Taiwan and across Asia builds deeper relationships, sharper insights, and opportunities that online meetings cannot fully replicate.

Your success is at the heart of what we do. We can’t wait to embark on this journey with you.

2. I already raised a Series A / I’m profitable, is AppWorks right for me?

The short answer is, yes!

The long answer is, reaching a funding goal can be a cause for celebration, but it’s also a relatively minor part of the founder journey. So many more things can go right or wrong, even with a funding round. There are many other facets to overcome and master. When we admit founders into the program, it is because we have carefully considered what they need as a founder, and how our resources and network across Asia can help them grow.

Joel Leong and Henry Chan atShopBackhad already built a business model and received seed funding in 2015 when they launched in Singapore before they came to AppWorks Accelerator #13 in 2016.

Joel told us that had the team known about Taiwan’s massive US$20 billion GMV e-commerce market and all the region-wide technical and tactical innovations that it would eventually yield, they would have made the move to Taiwan much sooner. Taiwan has since become one of ShopBack’s biggest markets and R&D centers. It demonstrates that funding rounds and business model maturity do not limit founders in learning something new.

As long as you think that AppWorks can help you in the entrepreneurial learning process, you should apply.

3. What is an RFS? What kind of support can AppWorks Accelerator provide for startups in AW#33 RFS#1: Manufacturing AI, RFS#2: Defense Tech, RFS#3: On-Chain Banking, and RFS#4: PQC?

A Request for Startups (RFS) highlights the specific problem spaces AppWorks is most focused on each batch – areas we believe have strong growth potential and for founders to make a meaningful impact.

A RFS is not a restriction; it’s a signal. It helps founders understand where AppWorks can provide the most value and resources in this batch. If you’re already building in one of these areas, we’d love to meet you. But even if not, as long as your startup aligns with our focus or could benefit from joining the AppWorks founder community strategically, you are very welcome to apply.

For AppWorks #33 (AW#33), we’re looking for founders building in Manufacturing AI, Defense Tech, On-Chain Banking, and PQC — four verticals that will redefine Asia’s industrial and economic foundation in the coming decade, and where Taiwan and the AppWorks community can provide a unique advantage.

AW#33 RFS#1: Manufacturing AI

Over the past two years, the rapid progress of AI has begun to fundamentally reshape manufacturing — from design and production to operation and maintenance. Now is the time for the industry to embrace intelligent transformation.

With Taiwan’s world-class manufacturing and supply chain ecosystem, AppWorks helps founders directly connect with leading OEMs, manufacturers, and cross-industry partners to co-develop and validate PoCs, as well as build AI-driven solutions for automation, quality inspection, and predictive maintenance.

Our community already includes startups deeply rooted in manufacturing innovation, such as NunoX (AW#31), which accelerates textile development with generative AI; Relajet (AW#17), which delivers advanced sound separation for smart acoustics; and Groundup.AI (AW#27), which enables predictive maintenance through acoustic monitoring.

Through collaboration, sales partnerships, and shared know-how within our network, AppWorks helps your solution validate faster, scale faster, and reach real-world impact.

AW#33 RFS#2: Defense Tech

In an era of geopolitical uncertainty and growing emphasis on supply chain and technological sovereignty, dual-use technologies such as unmanned systems, sensing, cybersecurity, AI models, and advanced materials are becoming critical to both national and industrial resilience. This shift is also creating unprecedented opportunities for startups innovating in high-barrier sectors.

AppWorks Accelerator, together with Wistron Accelerator, has long focused on hardware, AIoT, and deep tech, providing a full-scale environment for manufacturing, prototyping, and validation.

Our community already includes deep-tech startups delivering cutting-edge solutions across both defense and commercial domains — such as Aliena (AW#30), developing propulsion systems for small satellites; Aonic (AW#30), Southeast Asia’s largest industrial and agricultural drone operator; and Mapxus (AW#30), offering precision mapping and geospatial intelligence.

Through this ecosystem, AppWorks helps founders connect with manufacturing and enterprise partners, develop and test PoCs, access investors and R&D talent, and accelerate both technological development and market adoption.

AW#33 RFS#3: On-Chain Banking

We believe the future of finance will be programmable, transparent, and borderless.

AppWorks is looking for founders reimagining financial infrastructure through Web3 technologies. From asset tokenization and decentralized clearing and settlement, to cross-border payments and on-chain compliance and regulatory tools.

As you build toward this new financial architecture, AppWorks helps you understand Asia’s fintech landscape, connecting you with regional financial institutions, compliance advisors, and investors.

Through our community of FinTech, LegalTech, and Web3 founders and mentors across nine markets in Asia, we provide hands-on insights and strategic guidance for scaling within regulated markets and driving real-world adoption. Our community already includes on-chain finance pioneers like StraitsX (AW#21), a MAS-licensed stablecoin infrastructure provider powering cross-border payments and regulated settlement across Asia.

AW#33 RFS#4: PQC

The cryptographic foundations protecting the global digital economy are mathematically vulnerable to quantum computers, and the threat is closer than most assume.

In March 2026, Google’s research showed that quantum computers may break today’s encryption with far fewer qubits than previously estimated, prompting Google to set 2029 as its internal PQC migration deadline. Meanwhile, “Harvest Now, Decrypt Later” attacks — where adversaries collect encrypted data today to decrypt once quantum capability arrives — are widely believed to already be underway.

Taiwan is uniquely positioned to lead this transition. Taiwanese semiconductor companies are already producing PQC-hardened hardware at scale: Winbond became the first memory vendor in the world to integrate PQC into its secure flash, now deployed across IoT, industrial, server, and automotive applications. AppWorks’ own community includes Chelpis Quantum (AW#10 / Wistron Accelerator #5), a PQC migration specialist already serving multiple financial institutions.

The verticals where PQC is most urgently needed: finance, telecom, manufacturing, and defense — map precisely onto AppWorks’ LP base and ecosystem. For founders building the security layer that every other industry will depend on, there is no better time, and no better place to start, than Asia right now.

Whether you’re building the next-generation AI factory, advancing dual-use technologies, constructing the foundation of on-chain finance, or pioneering the quantum-safe security infrastructure of tomorrow, AppWorks is more than an accelerator — we’re your strategic partner for entering Taiwan and scaling across Asia. Helping you go from prototype to scale, from the lab to the real world.

4. How can AppWorks Accelerator help a web3 founder?

a. Grow with one of the largest web3 founder communities.

AppWorks has built a Web3 ecosystem of more than 152 active teams and 313 founders. Our accelerator alumni includePendle (AW#20), a DeFi yield-trading protocol enabling the tokenization and trading of future yield, andStraitsX (AW#21), a MAS-licensed stablecoin infrastructure provider powering cross-border payments and regulated settlement across Asia. Beyond our accelerator alumni, our fund portfolio includes Sanctum, the largest Solana liquid staking token infrastructure with 16.25M SOL (US$1.45B) under management, and SignalPlus, a leading platform for digital asset options trading.

b. Build PoC and product integrations with key Web2 and Web3 partners.

Through deep collaborations with leading financial institutions, telecom operators, and exchanges in Taiwan, AppWorks provides Web3 startups with real PoC opportunities to test and refine products in a trusted and compliant environment. Beyond Web3, our large Web2 founder community spanning B2C and B2B sectors offers potential partnerships that help you reach new user profiles and accelerate adoption.

c. Stay ahead of the game to capture the pulse of the ecosystem and access premium development partners

Within the AppWorks community, nearly 95 teams are already building on major public chains such as Ethereum, Solana, Arbitrum, Hyperliquid, Sui, and Base.

We maintain close ties with leading L1 and L2 ecosystems, and partner with global blockchain infrastructure players including GSR, Alchemy, Quantstamp, and Chainlink, ensuring founders can access reliable tools, liquidity partners, and expert support to scale faster in the region.

5. How does AppWorks Accelerator help founders enter new markets?

Since 2010, AppWorks has made close connections within founder communities and throughout the venture capital ecosystem. When startup teams decide to enter a new market, we can quickly help them learn from local partners to tap into key resources and business models that are specifically tailored to different regions.

Today, the AppWorks community brings together over 600 active technology startups, of which more than 300 operate across multiple Asian markets. The network spans founders from Singapore, Indonesia, Vietnam, the Philippines, Malaysia, Korea, Japan, Hong Kong, and Taiwan—ensuring that wherever you plan to expand, there’s already an AppWorks founder community on the ground ready to exchange insights, share local know-how, and open doors.

This community is supported by a strong layer of mentors, alumni founders, and seasoned operators, many of whom have built, scaled, or exited successful companies. Together, they form a trusted network that helps new founders navigate everything from product localization to cross-border partnerships.

Beyond the founder network, AppWorks actively invests in over 25 venture funds across AI and Web3, including AC Ventures, Golden Gate Ventures, Openspace Ventures, Ascend Vietnam Ventures, Figment Capital, and Pantera Capital. This extended capital network gives founders exposure to top investors and potential follow-on funding partners throughout Asia.

AppWorks also partners with leading corporate LPs across manufacturing, finance, media, and telecommunications. Our funds are backed by institutions such as Malaysia’s sovereign wealth fund and Korea’s government investment agencies, giving our founders privileged access to regional corporates, pilot opportunities, and distribution networks.

6. What does AppWorks look for in applications?

When AppWorks reviews applications submitted by founders, we pay special attention to a founder’s north star. Some questions that might help you think about whether AppWorks is a good fit for you:

Why did you launch your startup?

What problem do you want to solve and why?

What do you believe fundamentally needs to exist in this world that doesn’t already?

What kind of future do you want to create and how will you get there?

What have you already done to demonstrate your commitment to tackling this problem?

AppWorks Accelerator’s online application covers about 30 topics related to team background, product/service, business model, market analysis, and more. It is very detailed and requires time to complete. It also includes a required one-minute self-intro from the founder (CEO) for us to know you better.

7. Does AppWorks Accelerator cost anything?

No. AppWorks Accelerator has always been free for founders. We will not charge rent or service fees, nor will we require any form of compensation, such as sweat equity, tokens, options, revenue, or profit-sharing. Our exclusive mission is to help founders.

8. We need funding now, can we get an investment by joining AppWorks?

The short answer is you will have much better access to us than non-AppWorks accelerated teams. We will discuss with you and help you figure out at this stage of your startup’s journey if capital can give your startup a significant edge and/or take it to the next level, or if there are other more burning issues, e.g., achieving stronger product-market fit, figuring out a working go-to-market strategy, recruiting a solid co-founder, etc.

Any AppWorks founder is welcome to start a discussion with us on fundraising anytime. We will do our best to advise and support you with US$ 386 million in total fund size behind us.

9. My service (or product) has not yet started to make money. Can I still apply?

Of course! There probably isn’t a better time to learn in an accelerator than as a founder just starting out. This period before a founder has built a startup into a scalable business model with Product-Market Fit is called the “seed stage.” During this period, founders always need more than funding; they need a variety of entrepreneurial-related insights, inspiration from other founders, and room for trial and error. AppWorks Accelerator, with over 15 years of experience, was built to provide these lessons and more.

10. I’m planning to expand my business into Taiwan, however, since I am not a Taiwanese citizen, can you help me obtain a proper visa?

International founders admitted to AppWorks Accelerator, according to your qualifications and needs, AppWorks can help with your application for theGold Card, or Entrepreneur Visa in Taiwan. This enables founders from overseas to concentrate on work in Taiwan without traveling abroad to sort out troublesome visa issues. We can offer guidance on this process.

11. Do I have to set up a company to join AppWorks Accelerator?

Not necessarily, but we recommend founders to set up an office when entering a new market, especially those of you that are B2B facing. This may enable you to build relationships with business partners and make negotiating commercial agreements smoother in the future.

For the founders who are planning to land in Taiwan, AppWorks has professional accounting and legal specialists who can assist in managing the necessary procedures, making the process of setting up much easier and more efficient.

12. What is the difference between applying during the first round vs. the final round?

The application period is split into two intakes, with interviews and admissions facilitated on a rolling basis. Based on past experience, teams that submit their application earlier tend to have a higher chance of being admitted and are also immediately granted access to all the resources that AppWorks Accelerator has to offer.

13. I have previously applied to AppWorks and have been rejected, can I apply again? Will it affect the chances of admission?

Reapplying represents the determination of the founder and is a positive signal for us. Therefore, we will re-evaluate all aspects, not only for the growth of the founder but also for the progress of the company. In the past, some entrepreneurs applied 2-3 times before being selected. In some cases, after unsuccessful applications, they continued to explore and eventually achieved more user growth and deeper insights. In other cases, they honestly faced the fact that there was no Product-Market Fit (PMF), changed their topic, found a scalable business model, and reapplied. These entrepreneurs have performed well after graduating from the accelerator.

We hope the above FAQ can help clarify your questions about AppWorks Accelerator. If you seek more clarity, please write to:[email protected], and we will try to answer your questions.

If you’re a founder creating what the world doesn’t know it needs yet, you’ve come to the right place! Applications forAppWorks #33 will be open until July 30, 2026. If you missed the deadline, join the waitlist for AppWorks #34