web3.GSEA Snapshot 2021 由 AppWorks 製作,有任何指教與建議,請 email 至 [email protected]。感謝以下 AppWorks 的朋友,在過程中提供的協助:Peter Ing (Co-Founder of BlockchainSpace)、Leo Pham (Manager of Access Ventures)、Hung Nguyen (CEO of Spores)、Tri Pham (CEO of Kardiachain)、Ben Minh Le (CRO of M3TA)、TN Lee (Co-Founder of Pendle Finance)、Lawrence Samantha (Founder of NOBI)、Eagle Su (Marketing Specialist of Zombit)

Jun is an Analyst covering both AppWorks Accelerator and Greater Southeast Asia. Born and bred in America, Jun brings a wealth of international experience to AppWorks. He spent the last several years before joining AppWorks working for Focus Reports, where he conducted sector-based market research and interviewed high-level government leaders and industry executives across the globe. He’s now lived in 7 countries outside US and Taiwan, while traveling to upwards of 50 for leisure, collectively highlighting his unique propensity for cross-cultural immersion and international business. Jun received his Bachelors in Finance from New York University’s Stern School of Business.

Founded in 2009, AppWorks is a leading startup community and venture capital firm built by founders, for founders. We are committed to backing the next generation of entrepreneurs in Greater Southeast Asia (ASEAN+Taiwan) and helping them to facilitate the region’s transition into the digital age. Building off the firm’s decade-plus of experience, AppWorks works closely with early-stage founders to achieve product-market fit, while helping growth-stage companies establish sustainable business models at scale.

Starting in 2018, blockchain was incorporated in the firm’s core mandate. We believe that the technology is currently driving a massive paradigm shift, opening up new disruptive and innovative opportunities for the next generation of entrepreneurs as the world transitions into the web3 era.

In 2021, blockchain entered a mass adoption phase. With the emergence of new innovative applications such as DeFi, NFTs, GameFi, and web3 infrastructure, an unprecedented number of new funds, retail investors, and users have flocked to the crypto world, creating a flywheel effect that has facilitated the formation of key web3 infrastructure that we believe will usher in a new era of large-scale commercialization.

“As the world decentralizes, will development vary between different countries and regions?” This is a question that we’ve mulled over years. With the accelerated development of blockchain, we recognize that, in fact, regional dynamics have become more pronounced. We found that in Greater Southeast Asia’s major markets, the confluence of different historical, economic, industrial, societal, and cultural contexts has resulted in crypto adoption taking different forms. The emergence of diversified crypto markets is driving growth in the region to meet different market conditions and leading to new business models and approaches in the industry that can be applied globally.

The following is an overview of our analysis and views on each major market in the region:

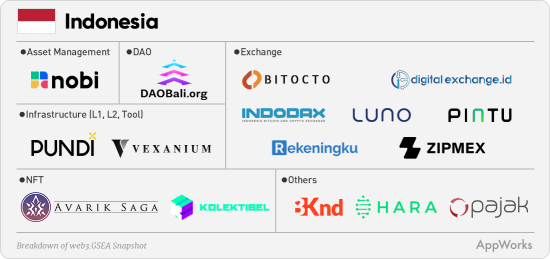

Indonesia: Crypto Investment Outstripping Public Equities

Indonesia, the world’s fourth largest population and the largest in GSEA, is estimated to have an unbanked population of 66%. Based on market size alone, Indonesia has become an important market for the development of blockchain. Indonesia is entering a financial paradigm shift driven by blockchain and cryptoassets, and overall development is trending towards exponential growth. According to statistics from Indonesia’s Ministry of Trade, during the first five months of 2021, more than 6.5 million people in Indonesia traded cryptocurrencies—far exceeding the 2.2 million who traded public equities—totaling US$25 billion in cryptocurrency transactions, compared to US$4.4 billion over the same period in 2020, representing year-on-year growth of 470%. With statistics like these, it comes as no surprise that cryptocurrency has become the most popular investment category among Indonesian retail traders.

Compared with other countries, the Indonesian government is relatively positive towards crypto. Since September 2018, a series of laws have been enacted, signaling the open attitude of the Indonesian government. The Commodity Futures Exchange Supervisory Board (BAPPEBTI) oversees cryptocurrency-related issues and has provided legal frameworks for licensing and trading. Currently, Indonesians can legally own and trade a total 229 different cryptocurrencies.

Indonesia’s crypto landscape is underlined by the rapid development and adoption of exchanges, wallets, asset management tools, and other DeFi applications. For example, Indodax, established in 2014, is Indonesia’s leading exchange with more than 4.7 million users. With increasing acceptance of investment in cryptocurrencies by the general public, new areas of development, such as investment platform NOBI, that provide asset management services that cater to crypto users will mark the next wave of growth.

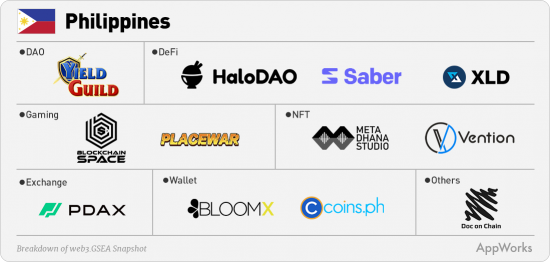

Philippines: Massive User-Driven Growth

In 2021, Yield Guild Games (YGG) broke out in the Philippines and became a global phenomenon. Evolving from its initial function of assisting Axie Infinity in recruiting and training players, YGG is now home to more than 1,500 NFT game guilds based in the Philippines. YGG provides players with digital asset management, game scholarships, and community support—becoming the world’s largest NFT gaming guild.

According to Playercounter, more than 40% of Axie Infinity players hail from the Philippines alone. Play-to-earn has proven to provide meaningful income to users, effectively alleviating economic pressure caused by the pandemic for many users.

This model of massive user acquisition to drive ecosystem growth is a unique characteristic of blockchain development in the Philippines. We anticipate that with the mass inflow of capital and users, there will be a corresponding entrepreneurial response that will lead to the creation of new and innovative applications in the Philippines. We have seen this trend emerge with projects like NFT marketplace Vention and gaming guild management and data platform BlockchainSpace.

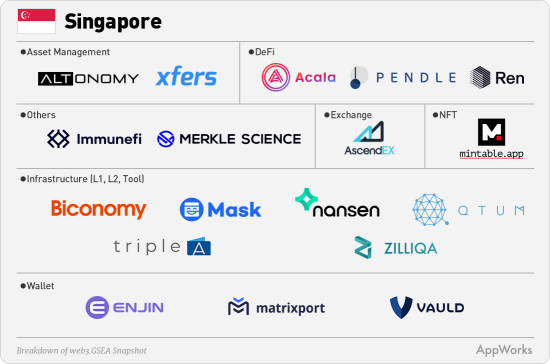

Singapore: Leveraging the Strength of Asia’s Financial Center

Singapore has always been known as Asia’s financial center, building off the government’s proactive policies over the past several decades. A similar trajectory is also taking shape in the country’s blockchain development. The Monetary Authority of Singapore (MAS) is the leading regulatory body overseeing cryptoassets, and has long demonstrated a relatively open and friendly stance on the development of blockchain and cryptoassets within the city-state.

As early as 2017, MAS issued “A Guide to Digital Token Offering” which established the Singapore government’s policy framework for ICOs, issuers and related platforms, under the purview of the Securities and Futures Act (SFA). In January 2021, the “Payment Service Act” (PSA) was launched, regulating all cryptocurrencies, exchanges, and digital payment services in Singapore.

As a result, there has been an emergence of several new blockchain-related applications. For example, Biconomy, which builds transaction infrastructure for blockchain applications and optimizes cross-chain transaction experience; Xfers, a developer of financial electronic payments; and Vauld, a service provider covering cryptocurrency transactions, lending, and wallets. In the future, we expect more projects coming out of Singapore in cryptocurrency-related asset securitization, license compliance, and international exchanges.

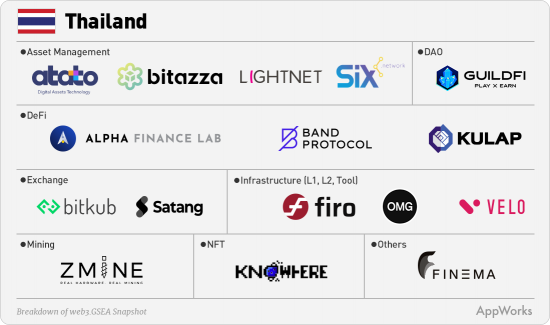

Thailand: From Late Mover to Frontrunner

While Thailand’s blockchain ecosystem can be considered quite early, 2021 marked an acceleration point with several milestones. In November, Thailand’s first blockchain unicorn was born as crypto exchange Bitkub sold a 51% stake worth US$535 million to Siam Commercial Bank. Paired together with logistics provider Flash Express’s newly minted billion-dollar valuation, Thailand welcomed its first unicorns of the internet and Web3 era respectively within a five-month period.

Bitkub’s success is galvanizing the Thai blockchain ecosystem, demonstrating that Thailand can develop scalable blockchain infrastructure. Bitkub alumni and seasoned Web2 entrepreneurs are diving into Thailand’s blockchain space, just as we’ve witnessed in other markets.

In fact, we can already see the emergence of more mature and advanced Web3 applications. For example, the emergence of cross-chain data oracle platform Band Protocol and metaverse gaming guild GuildFi show the level of innovation and reiteration happening in the market. We believe that in the near future, we will see more projects in the NFT space, building off Bangkok’s rich fashion and design industry and the country’s active NFT artist community.

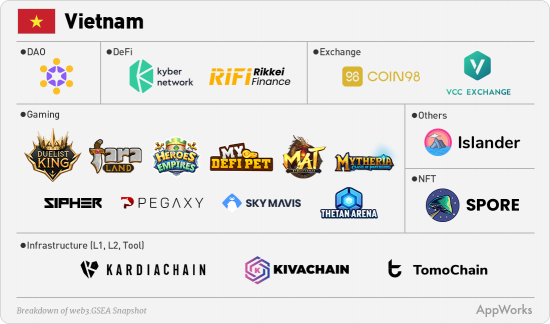

Vietnam: The Axie Infinity Effect

When it comes to Vietnam, the most well-known player is Sky Mavis, the developer behind the killer NFT-based game Axie Infinity. According to CryptoSlam statistics, since its launch in 2018, the total amount of NFT transactions on Axie Infinity reached more than US$3.7 billion, with more than two million daily active users, culminating in Sky Mavis’s recently completed US$152 million Series B round of financing.

The impact of Sky Mavis’s success on Vietnam can be observed from two perspectives. First, it is driving the growth of Vietnam’s local NFT gaming ecosystem and attracting international capital to accelerate development and adoption. For example, in October, Sipher raised US$6.8 million in seed financing from major global investors. In addition, there’s been a surge in casual and semi-casual GameFi projects coming out of the woodwork including My DeFi Pet, Mytheria, Thetan Arena, and Faraland.

Second, Vietnamese users have demonstrated high levels of acceptance for blockchain and cryptoassets. According to the 2021 Global Crypto Adoption Index survey conducted by Chainalysis, Vietnam ranked first globally in terms of overall adoption. Among three indicators, on-chain value received, on-chain retail value received, and P2P exchange trade volume, Vietnam ranked in the top five in the world. We anticipate that new applications in DeFi, wallets, and asset management like we see with Kyber Network’s Liquidity Hub will highlight the next wave of blockchain innovation in Vietnam.

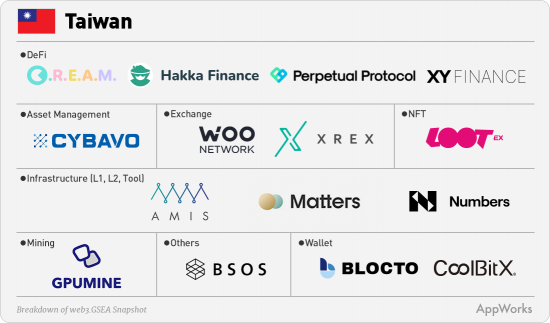

Taiwan: A Huge Digital Market Driven by Engineering Talent

Compared with other markets in the GSEA region, Taiwan has two notable characteristics and advantages in blockchain development. First, Taiwan is home to a massive digital gaming and entertainment market. To illustrate this market size, according to App Annie, in 2020, Taiwanese consumers spent US$2.44 billion in the App Store, equal to total spending from Indonesia, Thailand, Vietnam, the Philippines, and Malaysia combined. Second, Taiwan has accumulated a wealth of engineering talent across manufacturing, software, and hardware integration. This talent pool has formed the core of Taiwan’s blockchain industry.

In 2021, Taiwan also joined the global NFT wave with early-stage activity. Leveraging the island’s fertile digital gaming and entertainment market, Taiwanese founders are adopting NFTs to create products, services, and new business models. Musicians, artists, game publishers, and influencers have embraced NFTs to build public awareness and tap into this new digital format of ownership, demonstrating immense promise for large-scale commercial adoption of NFTs.

Since the advent of Ethereum, Taiwan’s local engineers have continued to explore the frontiers of blockchain development, becoming a key driving force in the crypto world. Taiwan is home to several notable projects led by seasoned teams, including Perpetual Protocol, which provides Virtual Automated Market Maker (vAMM) to implement perpetual contract solutions; smart contract wallet Blocto has become the go-to wallet for Flow—with more than 80% of Flow users trusting Blocto for Flow Token pledges. In cross-chain applications, Blocto also supports Ethereum, BSC, Solana, Avalanche (c-chain), and Polygon, among other mainstream public chains.

Bright Days Ahead

Just a few years ago, you’d be hard pressed to find the words web3, blockchain, DeFi, or NFTs uttered anywhere outside of niche crypto spheres in this part of the world. Now, sentiment from founders and investors across the region have evidently shifted from “why web3?” to “how do I get a piece of it?”—largely in this past year alone.

Taiwan is at the forefront from a technical perspective, with an unparalleled engineering pool in terms of cost and performance; Indonesia is emerging as massive market for web3 consumers, now with crypto traders outnumbering stock traders by severalfold; Philippines is in a close second, with everyday users showing an uncanny demand for GameFi to make ends meet; Thailand’s historically nascent ecosystem is expected to garner significantly more attention now with their first crypto unicorn; Vietnam, given Axie’s success, is quickly distinguishing itself as a the world’s NFT gaming hub; and lastly, Singapore’s position as the region’s financial and management hub will likely extend into the web3 era.

Any doubts of whether or not web3 is here to stay were certainly eroded by the massive strides that the regional ecosystem has taken in 2021. Looking forward, the development and adoption of web3 is looking especially bright. Although crypto markets will likely ebb and flow in the coming months and years, with the occasional bears and dips, many stakeholders across the value chain have already gotten taste, and will likely only want more.

The 2021 Greater Southeast Asia Blockchain Ecosystem Map is authored by AppWorks. For inquiries, please write to [email protected]. For this survey, thanks for several friends’ assistance: Peter Ing (Co-Founder of BlockchainSpace), Leo Pham (Manager of Access Ventures), Hung Nguyen (CEO of Spores), Tri Pham (CEO of Kardiachain), Ben Minh Le (CRO of M3TA), Rémy Perettieny (CEO of Reminiscense), TN Lee (Co-Founder of Pendle Finance), Lawrence Samantha (Founder of NOBI), and Eagle Su (Marketing Specialist of Zombit)

【If you are a founder working on a startup in SEA, or working with AI, Blockchain, and NFT, apply to AppWorks Accelerator to join the largest founder community in Greater Southeast Asia.】

David is an Associate mainly focused on investments. He previously lived in the US, but was drawn to the Greater Southeast Asia region by the growth opportunities and the wonderful people here. He spent the first five years of his career as a consultant at IBM, where he became intimately familiar with the enterprise software and services needs of Fortune 500 companies. Later, he focused on building predictive models and solving optimization problems for large companies, and gained an appreciation for the role of data and algorithms in our lives. He joined AppWorks in 2020 after receiving his MBA from Columbia Business School, and also has a B.S. in Mathematics from the Ohio State University. In his free time, he tries to stay active and is always looking for opportunities to hike or trek, often seeking the trail less traveled.

2021 was a banner year for retail cryptocurrency adoption. The most exciting up-and-coming projects and meme coins alike have entrenched themselves into dinner table conversations for tens of millions of retail users, while the Coinbase IPO legitimized the space for many institutional observers.

However, remarkably, we are still in the early stages of development in other segments of the crypto space. The first wave of institutional investors have been around for a while, but it’s still a drop in the bucket for traditional institutions managing trillions of dollars in assets.

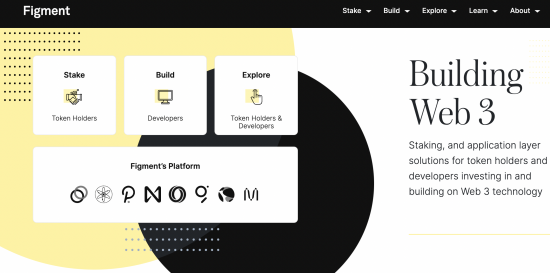

Today, we announce our investment into Figment, one of the largest independent enterprise staking service providers in the world. Of course, at AppWorks, no investment could be made without having strong conviction in the founding team, and we found an exceptional founder in Lorien Gabel.

A serial founder with the heart of a warrior

When we first met Lorien we could immediately feel a calm sense of depth, wisdom, and ambition. A veteran founder of the web1 era, which enabled millions of ordinary people to publish and read content on open protocols, Lorien has long been fighting for and brings a special passion for the principles of decentralization.

And with three successful exits under his belt, Lorien brings more than a few battle scars as a tech entrepreneur. He built the first of his many ventures, one of the early internet service providers, with his brother in their 20s, before being acquired by what became the largest consumer ISP in Canada. Their second company, a web hosting service, was another early mover in the web1 days and was acquired by AT&T Canada. And now they’re back at it again with Figment.

Despite being told by many investors early on that he was building a commodity business, Lorien never gave up, taking it on as a personal challenge to emerge from the pack while always keeping an eye on the long game. In hindsight, it is not the least bit surprising that he and his team have been able to build a unicorn in just a few short years.

But Lorien isn’t stopping here. While the results thus far speak volumes, we are even more impressed by his determination to take Figment into the future. We weren’t surprised to hear that the team never even considered recent acquisition offers, given Lorien’s passion for solving intellectually challenging problems, his warrior-like mentality towards finding a way to emerge from a highly competitive landscape, and his sheer drive to create outsized impact in the web3 ecosystem.

Exploding demand for staking as crypto is legitimized

Figment provides staking infrastructure for institutional asset holders and custodians, allowing crypto asset holders to earn yield by participating in the upkeep of the network. Tokens belonging to this exploding asset class, proof-of-stake tokens, utilize a more environmentally-friendly consensus mechanism while generating yield for holders.

Staking is not a trivial task and involves frequent node infrastructure updates. High performance and execution is required, as nodes that do not perform as expected are punished financially, hurting staked token holders. As one of the largest players in the space, Figment has the resources to deploy teams of researchers and engineers to ensure high performance across several chains and play a critical role in the governance of each chain.

As staking service providers consolidate into a small handful of dominant players in a market expected to reach US$50 billion in just a few years, we believe in Figment’s ability to emerge as one of the top players and create tremendous value, something we have already recognized as a loyal customer ourselves.

Unlocking the next frontier

We’re excited to see how Figment will evolve under Lorien’s leadership, and we have a feeling that the business will look very different in five to ten years, as any great business does. As an operator of node infrastructure, they are in a unique position to offer indispensable services to web3 developers just as the developer flywheel is beginning to take off. Figment has already demonstrated remarkable promise in their web3 explorer Hubble, developer platform DataHub, and search service.

At AppWorks, we look for great founders who seek to create significant impact and move their respective industries forward. We’re honored to have the privilege to partner with Lorien and the entire Figment team as they continue to push the envelope on enterprise-grade staking and the rapidly evolving web3 development landscape.

【If you are a founder working on a startup in SEA, or working with AI, Blockchain, and NFT, apply to AppWorks Accelerator to join the largest founder community in Greater Southeast Asia.】

TAIPEI, TAIWAN—On December 21, 2021, AppWorks Accelerator held its 23rd demo day virtually, unveiling 23 startups operating across the frontiers of AI/IoT, Blockchain, and Southeast Asia. The event is held in collaboration with AWS Activate, with support from Google Cloud, Flow, and Alchemy, and promptly follows the firm’s in-person demo day held on December 15 specifically for those teams in the batch targeting the Taiwan market.

As one of Greater Southeast Asia’s longest running independent accelerator programs, AppWorks Accelerator built off the success of AW#22’s fully virtual Demo Day earlier this year, attracting innovative founders from around the world. The event will be broadcasted live across the firm’s Facebook page and YouTube channel at 09:00am Taipei Time (GMT +8).

AW#23 officially kicked off in September 2021, featuring 34 teams and 66 founders from 16 different home markets, including Australia, Hong Kong, India, Russia, Singapore, Taiwan, Thailand, the United States, the United Kingdom, and Vietnam. Reflecting the global embrace of digital work, 67% of the teams are internationally-based outside of Taiwan.

As an early mover in Blockchain and NFT investments, AppWorks proudly presents 11 DeFi- and NFT-related projects to showcase their products on the virtual demo day, leveraging the firm’s extensive experience in cryptocurrency to provide guidance and best practices in the space. Eight startups addressing dynamic opportunities in the Greater Southeast Asia region were represented in the batch, targeting verticals such as D2C brands, gaming, proptech, retail & e-commerce enablement, and more.

AppWorks is currently accepting applications for AppWorks Accelerator Batch #24, accepting qualified founders in AI/IoT, Blockchain/NFT, and Southeast Asia-related startups. AW#24 will be held from March to July 2022. The accelerator is equity- and cost-free, providing practical and hands-on mentorship to guide founders in achieving better product-market fit, win key business partners, and become a better founder.

For AW#23, the accelerator featured the following companies:

YouHomes: An all-in-one cloud based application to help real estate brokers save 50% operating cost and increase 30% sale transactions

The AppWorks Ecosystem Galvanizes in the New Digital Age

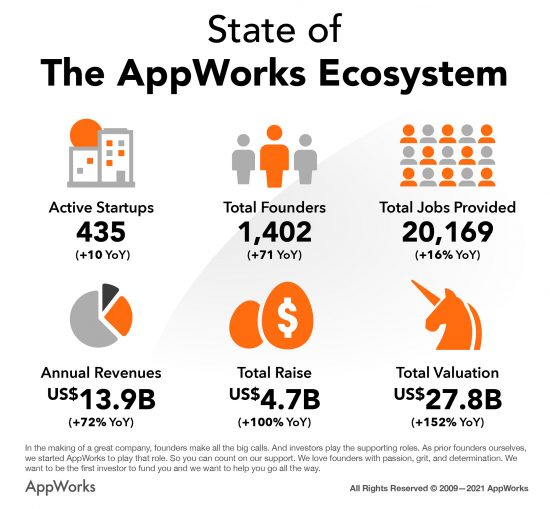

As one of Greater Southeast Asia’s largest accelerator programs, AppWorks holds its Demo Day twice a year, welcoming investors and business leaders seeking partnerships with carefully selected digital innovators from across the region and around the world. With the addition of AW#23, there are now 435 active startups and 1,402 founders in the community. Both the total funds raised and valuation have more than doubled in the last year. The AppWorks community now accounts for US$13.9 billion in annual revenues, creating over 20,000 high quality jobs in the digital economy.

“Our mission has always been to help founders be the best they can be, capitalize on mega paradigm shifts and maximize their impact on Taiwan and Southeast Asia. At this current stage, we are most optimistic about the disruptive potential of AI, blockchain/NFT, and SEA (ABS). We are at the cusp of the web3 revolution. 20 years from now, a few of the web3 startups or “DAOs” will become killocorns, and dozens will turn into hectocorns. Many of them can and will be born out of Taiwan and Southeast Asia. When that day comes, I am not sure where today’s tech giants or financial empires will be. Many might have fallen like what AOL, Yahoo and Nokia did. There’s really no better time to be a founder. AppWorks will be here to help them on this long journey, become the best founder they can become and build the most impactful startups/DAOs they can build,” said Jamie Lin, Chairman and Partner of AppWorks.

【We welcome all AI, Blockchain, NFT, or Southeast Asia founders to join AppWorks Accelerator】

AppWorks

Founded in 2009, AppWorks is a leading startup community and venture capital firm built by founders, for founders. We are committed to backing the next generation of entrepreneurs in Greater Southeast Asia (ASEAN+Taiwan) and helping them facilitate the region’s transition into the digital age. Just as how mobile and the internet completely transformed the status quo, we believe the current era of technology is currently being defined by major three paradigm shifts: AI, Blockchain, and Southeast Asia (ABS).

As such, whether it’s mentorship, investment, or talent, AppWorks has established a one-stop-shop for ambitious founders willing to bet against the consensus and drive a change they want to see in the world. We help startups build disruptive businesses from even an inkling of an idea into world-class enterprises through our three primary lines of service: Accelerator, Funds, and School.

AppWorks Accelerator is a launchpad for bold and ambitious entrepreneurs targeting Greater Southeast Asia (GSEA). Every six months, we take in startups with strong potential, equipping founders spanning all walks of life with the necessary resources, mentorship, and guidance to get their ventures off the ground.

There are now a total of 435 active startups and 1,402 founders in the AppWorks Ecosystem. Collectively, all companies produce a turnover of US$ 13.9 billion, an annual increase of 72% compared to the same time last year, and provide 20,169 jobs, 16% more than the year prior. Altogether, the Ecosystem raised a total of US$ 4.7 billion, an annual increase of 100%, with an aggregate valuation reaching US$ 27.8 billion, growing 152% YoY.

AppWorks manages three venture capital funds totaling US$ 212 million. We’ve attracted a diverse array of LPs who believe in our vision, including Taiwan Mobile, Axiom Asia Private Capital, Fubon Life, Wistron, Cathay Life, and Taiwan’s National Development Fund. We fund 20 deals a year, now with more than 70 names in our portfolio, including leading startups in several verticals such as Lalamove, Dapper Labs / Flow, Animoca Brands, 91APP, Carousell, ShopBack, Tiki, 17LIVE, and KKday, while having produced 5 IPOs, 2 IEOs, 1 hectocorn, 2 decacorns, and 4 unicorns.

Established in 2016, AppWorks School has strived to cultivate a pipeline of skilled engineers to help our community meet the technical demands of tomorrow. Quality talent has always served as the bedrock of innovation, yet shortages still remain the foremost challenge that tech companies in GSEA face today.

Within five years, AppWorks School has graduated 352 aspiring software engineers; 90% of these graduates went on to pursue successful software development careers in prominent companies such as momo, 91APP, KKBOX, WeMo Scooter, and Gogoro. AppWorks School currently provides five courses: Android, iOS, Front-End, Back-End, and Data Engineering.

In mid-December, we hosted an in-person Demo Day in Taipei, Taiwan, featuring startups that are facing the Taiwan market. And we thought it would be great for the founders to showcase their product and team to the wider startup community from the region through a virtual Demo Day.

This past half year, AppWorks Accelerator recruited 34 teams across AW#23, of which 8 are focusing on NFTs specifically, while 5 teams are focusing on DeFi / other blockchain solutions, 11 teams on Southeast Asia, and 14 teams on AI/IoT. It is one of the largest and most diverse batches to-date, with 66 founders in total who span across 16 different nationalities. Over 20% of them are women and 45% of the founders are serial entrepreneurs.

This particular demo day will feature 23 startups, with many in the NFT / blockchain space to give you a glimpse into our digital future. Tune into our livestream on YouTube or Facebook at 9 am (GMT+8) December 21st.

You can find a brief introduction to each pitching team and founder below:

If you are an investor or corporate representative and need more detailed information about the teams or want to connect with AW#23 founders, please email us at [email protected].

We welcome all AI, Blockchain, NFT, or Southeast Asia founders to join AppWorks Accelerator.