這股對於「動員群眾,齊心達成目標」的信念及熱愛始終如一,但 Tim 對於政治的想法隨後發生了改變。身為少數族裔,看著茶黨運動(Tea Party Movement)重塑美國政治版圖,Tim 開始思考:從政真的是他能發揮最大影響力的一條路嗎?

帶著這樣的疑問,他跟隨同儕來到矽谷,並在普林斯頓大學就讀期間,透過引薦認識了 Jack Dorsey 並加入 Square。這段經歷徹底改變了他的視角。他意識到,打造一家公司和打一場選戰的驅動力如出一轍:一個值得解決的問題、一股支撐你走下去的強大信念,以及號召眾人與你同行的能力。唯一的差別是,商業世界的反饋速度快多了。

從父母的地下室走向紐約證交所

2013 年,Tim 與共同創辦人 Jonathan Chen 拿著 Plug & Play 的一筆小額種子資金,創辦了政策與市場情報 SaaS 平台 FiscalNote。在初期為了省錢,公司註冊地直接登記在 Tim 父母的地下室,整個創辦團隊更是擠在一間狹小的 Motel 6 的房間內長達數個月,只為打造出 MVP。之後,在急需資金又欠缺人脈的情況下,他們在某天半夜寄了一封 cold mail 給知名投資人 Mark Cuban,沒想到 Cuban 馬上回信。這封信件隨後開啟了一場長達六小時的即時 Due Diligence ,面對許多沒準備過的問題,兩位創辦人甚至得臨場即興發揮才能招架他犀利的提問。但這招奏效了,Cuban 最後決定投資 FiscalNote。

2018 年完成 D 輪融資後,FiscalNote 迎來了與經濟學人集團旗下 CQ Roll Call,也是 FiscalNote 主要競爭對手的正面對決。Tim 找上一位與著名的羅斯柴爾德家族(同時也是經濟學人集團大股東)有交情的大學好友,成功約到了 CQ Roll Call 的執行長。對方以為這只是一場前輩指導後輩的閒聊,不料 Tim 直接攤牌:若不把數據部門賣給 FiscalNote,就準備迎戰一個資金充沛、且產品明顯優於 CQ Roll Call 的強勁對手。這場會面結束後,那位執行長帶走了一份被收購的投資意向書。最終,收購案順利落幕,奠定了 FiscalNote 在產業中的霸主地位。2022 年 8 月,公司正式在紐交所掛牌上市,如今服務全球超過 6,000 家機構,涵蓋過半的財富 500 強企業與破千個美國聯邦政府機構。

公司成功上市後,Tim 轉換了自己的角色,開始經營一家橫跨金融科技、國防與氣候科技的 Venture Studio。儘管有趣,但他總覺得少了點什麼。經過一段時間的探索後 Tim 才找到答案:他懷念那種捲起袖子在第一線拚搏的實戰感。與此同時,上述提到美國診所體系中的不效率,作為他職涯中所見過最大的未解難題,不斷在他眼前浮現。於是,他與 Jonathan Chen 再次聯手創立 Nitra。

醫療產業看似遙遠,但 Tim 在 FiscalNote 累積了十年的實戰經驗完美契合醫療市場的特性:如何贏得非科技原生傳統機構買家的信任、駕馭與合規高度相關的工作流程,並開發出能無縫融入日常營運的軟體。政府機構、律師事務所和醫療診所其實非常相似:它們都是在繁瑣法規限制下運作的專業服務機構,任何帳務疏失都會帶來財務與合規的雙重災難。當 Tim 和 Jonathan 重新踏上旅程打造 Nitra 時,他們帶著的是在 FiscalNote 打磨了十年的歷練。

In US outpatient care, the limiting factor isn’t capital. It’s the operational drag. Physicians and clinic administrators spend up to a third of their work hours on non-patient-facing tasks, and a significant share of that burden falls on financial operations. Multiply that across 350,000+ independent group practices in a $5.9T market, and the problem becomes staggering. The tools available to most practices were never built for them. The entire stack — expense platforms, accounting software, procurement systems — was architected for a different kind of company, and practices have been patching around that mismatch ever since.

Nitra was founded to close that gap. The company provides an all-in-one finance and workflow platform for US practices: a healthcare-native credit card, expense management, bill pay, and a procurement marketplace aggregating 350,000+ medical SKUs.

Indeed, a $5.9T market is exciting, but markets don’t build companies. Underlying our thesis is Timothy Hwang — a founder who has already navigated the full journey from a shared Motel 6 room to the NYSE, and came back to do it again on one of the hardest problems in American healthcare.

From Capitol Hill to Silicon Valley

Before startups, Tim’s early ambitions were in politics. Growing up in Washington, D.C., he started a peer-to-peer tutoring nonprofit as a teenager, donating the proceeds to purchase school supplies for children in need. By eighteen, he had run for the county’s board of education and won—38,000 votes, a $500M budget, and responsibility for 60,000 employees. He later joined the Obama presidential campaign as a regional field organizer. Politics, for Tim, was never abstract. It was a system for mobilizing people toward a shared goal at scale.

That certainty about mobilizing people never left him—but the arena shifted. As a minority watching the Tea Party Movement reshape American politics, Tim began to question whether elected office was the highest-leverage path available to him. He followed his cohort to Silicon Valley, joining Square through an introduction to Jack Dorsey while still studying full-time at Princeton. What he found there reframed everything. Building a company, he realized, ran on the same fuel as a political campaign: a problem worth solving, a conviction strong enough to sustain you, and the ability to get people to move with you. The feedback loop was just much faster.

From Basement to NYSE

Tim and his co-founder Jonathan Chen received a small check from Plug & Play to kickstart FiscalNote, a policy and market intelligence SaaS platform, in 2013, registering the company in his parents’ basement and sharing a Motel 6 room to survive. Needing funding with no warm intros, they cold emailed Mark Cuban in the middle of the night. Cuban replied instantly, and what started as an email exchange turned into a six-hour live due diligence session, with the two founders making things up on the spot to keep up with his questions. It worked. Cuban invested. From there, that scrappy, fearless energy never left the company: FiscalNote scaled quickly, growing to a team of more than 200 in under five years and reaching eight figures in revenue.

After its Series D in 2018, FiscalNote was going head-to-head with The Economist Group’s CQ Roll Call. Tim tracked down a college friend with ties to the Rothschild family, a major shareholder of The Economist Group, and secured an introduction to its CEO. The CEO arrived expecting a mentorship chat; Tim arrived with a choice: sell the data division, or face a well-funded, tech-native competitor. The CEO left with a term sheet. The acquisition followed, cementing FiscalNote as the dominant player in its category. In August 2022, the company went public on the NYSE, and today serves over 6,000 organizations globally, including more than half of the Fortune 500 and over 1,000 US federal government agencies.

After FiscalNote’s listing, Tim ran a venture studio across fintech, defense, and climate. He found it stimulating, but something was missing: the grind. Healthcare kept surfacing as the largest unsolved problem in his orbit, and he and Jonathan regrouped to build Nitra. The move made more sense than it looked: Tim’s decade at FiscalNote had given him a transferable playbook for exactly this kind of market: earning trust from institutional buyers who aren’t technology natives, navigating compliance-adjacent workflows, and building software that embeds into daily operations. Government agencies and law firms are not so different from healthcare practices: professional services businesses inside a regulatory maze where billing errors carry both financial and compliance consequences. When Tim and Jonathan sat down to build Nitra, that playbook came with them.

Why Nitra? Why Now?

Three years since launch, the numbers are compounding. Nitra has onboarded 700+ practices, grown quarterly GTV 9.3x year-over-year, and is seeing a growing share of those practices adopt multiple products across its financial back office, with the card as the entry point, expense management, bill pay, and procurement building on top.

The forward-looking question is what this platform looks like with AI on top — and Nitra is already answering it. Today, Nitra AI agents already handle tasks across the platform, from issuing virtual cards, placing procurement orders, to surfacing expense anomalies in one conversation, while voice AI for patient scheduling and agentic modules for clinical workflow are on deck for 2026. Underneath all of it, the platform is capturing what no generalist fintech ever could: every dollar moving through a practice, tied to a vendor, a drug, a procedure. The long-term vision is a full CFO and operations layer woven into how a clinic runs. Practices have spent years stitching together tools that were never built for them. When the infrastructure is finally purpose-built, they stop patching, because they no longer need to.

The AI era is also accelerating how quickly underdigitized industries can adopt software — and healthcare is one of the largest of them. Tim has a direct track record of navigating exactly this dynamic: FiscalNote brought data intelligence to government agencies, congressional offices, and law firms. All of them were institutional buyers operating inside regulatory constraints, largely unfamiliar with software, and skeptical of change. He learned how to earn their trust, embed the product into daily operations, and scale from there. That experience maps directly onto what Nitra is building.

The market is large, the timing is right, and the product is already working. Underlying all of it is our founder bet. Tim and Jonathan chose to return to zero after a public exit, picked one of the most structurally complex markets in the US economy, and are building with the same scrappiness and significantly more accumulated wisdom. The fact that Tim has already taken a company from his parents’ basement to the NYSE, and came back for something harder, tells us more about what Nitra can become than any market sizing exercise. We are proud to support them on this second, more ambitious journey.

We are delighted to share that AppWorks has invested in $CLOUD, the native token of Sanctum, as a demonstration of our long-term belief in Sanctum’s founding team and in the strong defensibility and moat they’ve built over the years.

Below, we will share why we think Sanctum is one of the most important companies being built on Solana; how it is reshaping one of the most misunderstood verticals in crypto, and why everything is finally clicking for them.

Sanctum – A Chronicle of Finding the Non Consensus and Right

To understand Sanctum, we need to first understand the history of Solana LST.

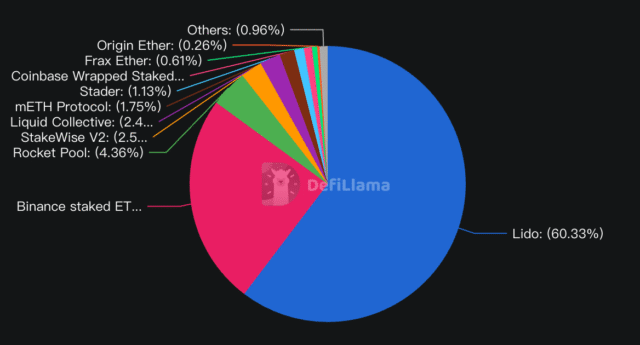

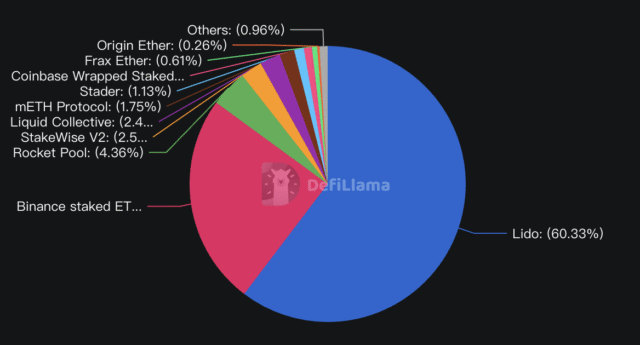

For the longest time, most people assumed Solana’s liquid staking market would follow the Ethereum playbook: one dominant player, i.e. Lido, and everyone else fading into the background. Many protocols rushed to build copycats of the Lido model, believing the game was simply about scale and validator sets.

Source: DeFillama

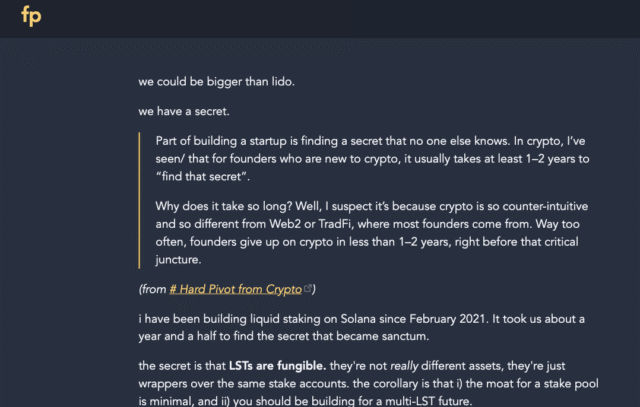

The most insightful founders see what others miss. FP Lee, Sanctum’s founder, being the core contributor who has designed Solana’s stake account contracts, knew early on that Solana’s setup is fundamentally different from Ethereum’s. Every stake account is modular, transferable, and composable. That means all LSTs on Solana are essentially fungible at their core. They are just wrappers of the same underlying stake accounts.

With that realization, the next question was obvious: in a world of many LSTs, what’s the missing primitive?

Look closely, stake pools serve three distinct purposes:

Delegate – achieve high staking yield and decentralize the network

Liquidate – Provide instant liquidity for staked SOL

And FP bet on liquidity.

Why? Because Ethereum already ran the experiment. Lido dominated Ethereum largely because stETH is integrated into all major DeFi protocols and has extremely high composability. Years of integrations made it the most composable asset on the network, and distribution compounded into dominance.

On Solana, the conclusion is even clearer. Stake accounts are interchangeable; every staked SOL carries the same economic weight in the transaction flow. In this world, a multi-LST future is the default, and whoever orchestrates liquidity wins the competition.

Therefore, instead of fighting to become the single biggest stake pool, FP saw a bigger opportunity in becoming the liquidity layer that unites all LSTs on Solana.

And this was the start of Sanctum.

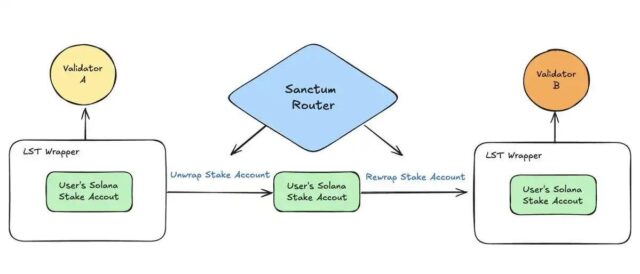

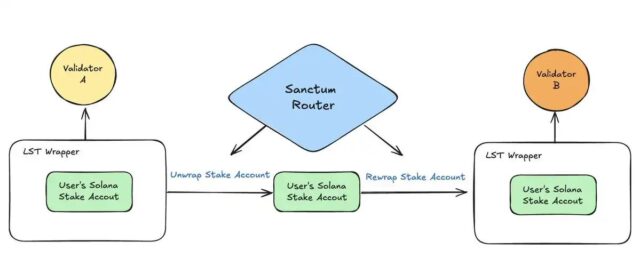

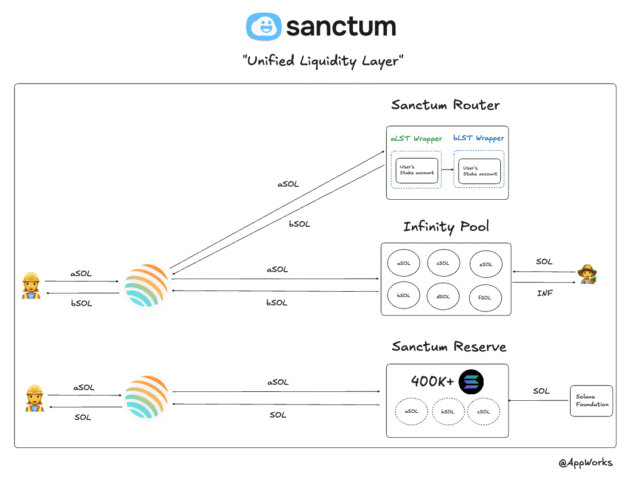

The way they cracked this is deeply connected to the insight. First, they created “Sanctum Router” for swaps between thousands of LSTs. A swap takes place with simply unwrapping and re-wrapping the underlying stake account.

Source: Sanctum document

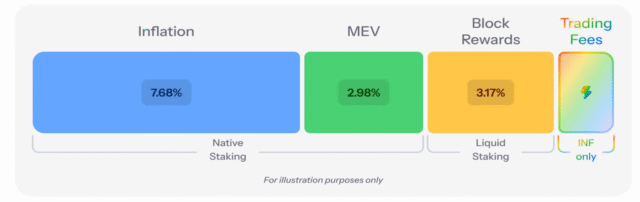

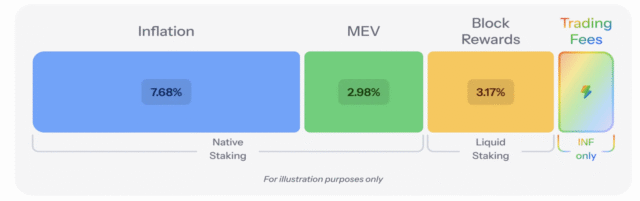

When necessary, swaps can also be routed into Infinity Pool, which can be regarded as a basket of LSTs that is managed by Sanctum, and all of these LSTs are under Sanctum’s flagship white labeled LST issuance infrastructure. When a swap is routed into Infinity, the trading fees are distributed to the liquidity providers of Infinity Pool, i.e. $INF holders.

This design reinforces liquidity for the entire Sanctum LST ecosystem while turning $INF itself into one of the most compelling LSTs on Solana.

Source: Sanctum document

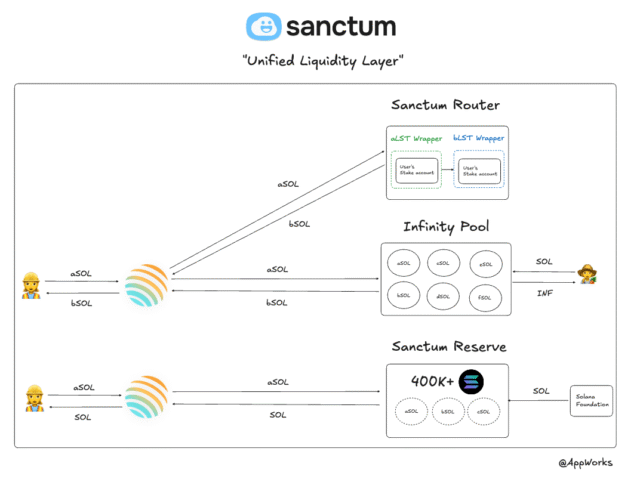

Lastly, a sizable native $SOL reserve managed by Sanctum is shared across all Sanctum branded LSTs. For any project, instead of spinning off another multi-million liquidity pool, they can just issue their LSTs with Sanctum without worrying about bootstrapping the liquidity.

Source: AppWorks

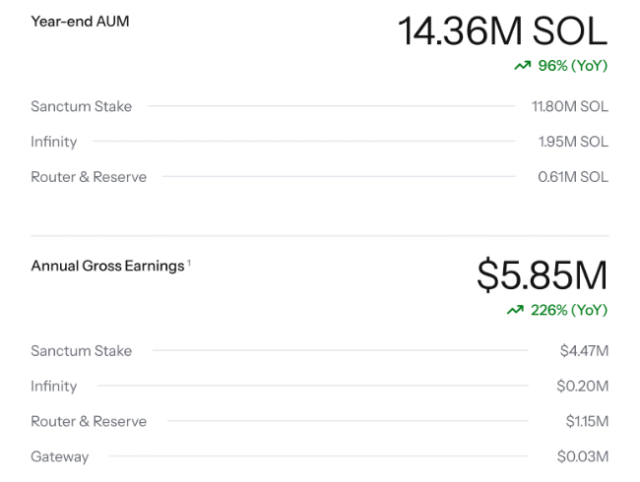

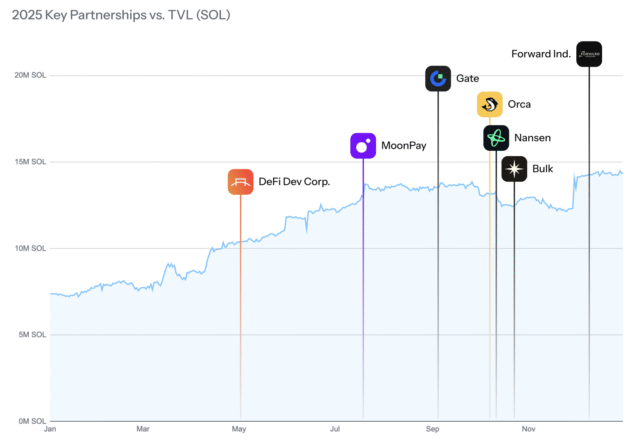

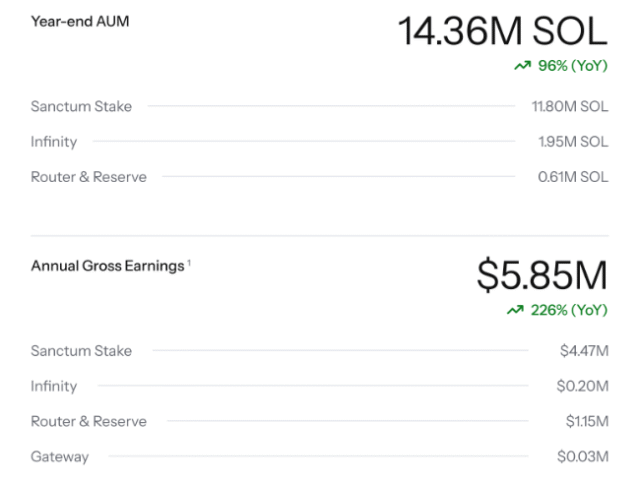

In less than 2 years, Sanctum is now managing over US$ 2B of $SOL with various key players in the space, including Bybit, Crypto.com, Backpack, Jupiter, etc. By the end of 2025, Sanctum closed the quarter with record-high metrics: 14.36M SOL (+96% YoY) under its umbrella and an annual revenue of US$5.85M (+226% YoY).

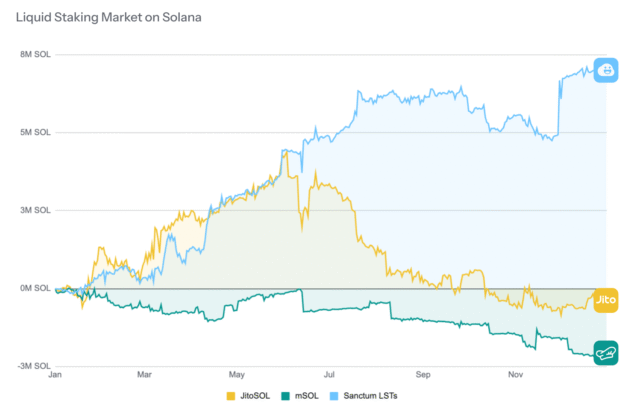

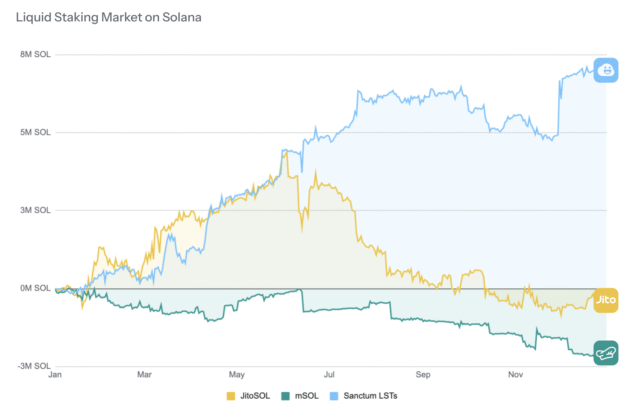

Another impressive metric to look at is Sanctum’s dominance of the Solana LST category in 2025; Sanctum achieved a net cumulative inflow of nearly 8M $SOL, while its two largest competitors, Jito and Marinade, saw their LST offerings end the year with net negative inflows. This disparity underscores the compounding competitive advantage of Sanctum’s liquidity moat within the LST market.

Source: Sanctum 25Q4 Report

Looking back, it is easy to think it was all smooth and inevitable, as if Sanctum’s rise was destined. But the truth is, this was the result of five years of persistence, iteration, and unshakable conviction through market winters. Every piece of today’s success was earned the hard way, block by block, decision by decision. And that leads us to our first and foremost thesis: the founderFP.

Thesis #1: Our core beliefs in FP Lee as a founder

Practiced Contrarianism

We see in FP that he has a unique ability to see what others miss and to dive deep enough into a concept until a contrarian insight emerges.

In 2023, while many were racing to build “the Lido of Solana,” FP noticed something upstream: Solana’s stake accounts were modular and fungible by design. That single observation flipped the playbook. Instead of competing to be the biggest pool, he built Sanctum as the liquidity layer that unites every LST, and that completely changed the game.

Source: 0xfp.com, 2023

And now, after years of living in Solana’s core, he’s spotted another inefficiency few others even noticed: the unreliable transaction layer. In short, we believe his latest move of acquiring Ironforge and launching Gateway reflects the same pattern: go deep enough, find the structural bottleneck, then build the missing piece of infrastructure that everyone else takes for granted.

Deep attachment to community

We believe founders’ ability to build a community in crypto is underrated. FP is one of the rare founders who doesn’t just “manage” a community but builds alongside them.

The Wonderland campaign, which Sanctum team held before their TGE, wasn’t just another points farm; Sanctum turned it into a coordinated, gamified quest layer where users stake LSTs to earn EXP and complete community challenges together, which kept participation sticky instead of mercenary.

The result was amazing, Sanctum’s TVL grew 171% in 38 days, and community forums spun up recurring events (like the Cloudfam Emoji Clan contests) that kept members creating and recruiting long after the initial drop, showing organic momentum rather than paid churn. Its community, later affectionately known as CloudFam, became one of the strongest grassroots movements on Solana.

Source: Sanctum website

What most people don’t know is how far FP and the team went to show that care. When it came time for the $CLOUD airdrop, they didn’t just run a script or crunch numbers in a spreadsheet. They manually sifted through thousands of Discord channels, Telegram chats to identify true evangelists and rewarded them far more generously than most projects would.

A token is ultimately a founder’s second product. Doing “token IR” right isn’t just about managing price; it’s about building trust, transparency, and belonging. Many founders say they care about token holders, but few actually walk the talk.

FP is one of those few that from publishing monthly updates to constantly engaging users in Discord, he treats community building like an ongoing craft. Over time, that level of authenticity compounds, turning a user base into something closer to a movement. We believe this will remain one of Sanctum’s strongest long-term differentiators.

Source: Sanctum $CLOUD holder group

Found his mission along the way

FP didn’t set out to be a founder. Before crypto, he was just a young software engineer trying to find his way. He stumbled into Solana out of curiosity and a desire for growth, and he stayed because, somewhere along the journey, he found meaning.

That meaning came from experience. After years of building in crypto, FP has seen it all — the FTX collapse, teams rugging their users, projects recklessly gambling away entire treasuries. In an industry often clouded by short-termism and greed, FP wants to prove that it is still possible to build a great product, stay transparent, and win the right way.

As intangible, and perhaps as cliché as it sounds, we believe this is one of the strongest forms of drive in the industry — and it is precisely the kind of mission we want to back.

Source: Solana Accelerate 2025

Thesis #2: Major upcoming catalysts for Sanctum LST

We see several catalysts for Sanctum LSTs, and we hold a strong conviction that everything is clicking for them now.

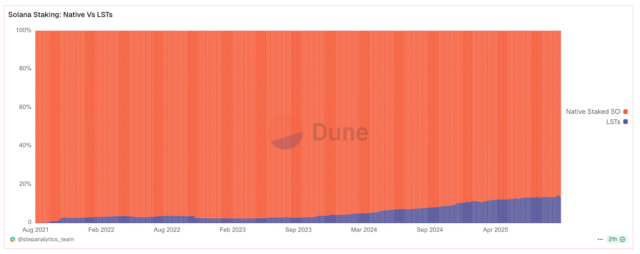

Solana LST is still early-stage and growing

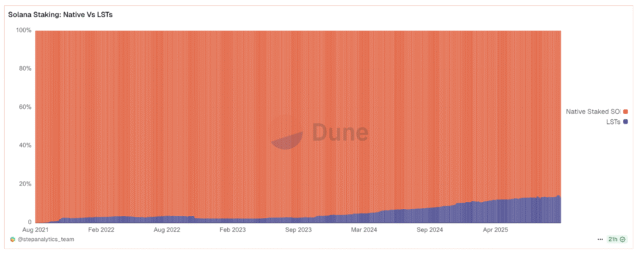

Solana’s liquid staking penetration has expanded 4.4x in two years, from 3% to 13.3%. This acceleration was actively driven by ecosystem catalysts like Sanctum and a growing appetite from validators to capture LSTfi market share.

Source: Dune

However, this 13.3% penetration implies that most of the staked $SOL remains illiquid. Drawing a parallel with Ethereum’s more mature market (approaching 35-40% LST penetration), it’s clear Solana’s liquid staking layer, the key to unlocking capital efficiency and composability, is still in its early innings.

We believe in this context, Sanctum is positioned right at that inflection point. Sanctum’s product suite (Router, Reserve, Infinity) is explicitly designed to be this non-partisan liquidity backbone. This creates a powerful moat, positioning Sanctum as the default aggregation point for a rapidly expanding and fragmenting market.

Network effects of LSTs

For any protocols that are launching a new LST, they don’t want to spin up multi‑million‑dollar liquidity pools. Instead, the easiest way is to plug into Sanctum, and focus solely on branding, core product, and distribution; Sanctum supplies the liquidity layer (Router + Reserve + Infinity) so these LSTs are interchangeable with the rest of Solana on day one. This is what we have been seeing. The alliance has been getting stronger and stronger every day. To date, Sanctum is serving all the biggest clients like Jupiter, Bybit, Backpack.

Source: AppWorks

More integrations → more supported LSTs → more interchangeable routes → deeper utility across DeFi.

That flywheel is hard to catch up to.

The Institutional Staking Layer

The competition for Solana’s yield is rapidly evolving beyond DeFi-native protocols. A new, larger wave of sophisticated capital, ranging from TradFi asset managers and potential SOL staking ETFs to publicly traded companies (like DATs), is now entering the arena.

For these entities, base staking yield is merely the starting point. To attract serious AUM, they must offer compliant, branded, and highly differentiated liquid products. This requires layering unique validator strategies, transparent reporting, and deep DeFi integrations on top of a base LST.

This is precisely where Sanctum becomes the critical enabling infrastructure. As a neutral, modular platform, it provides the full-stack “Staking-as-a-Service” for any entity to launch its own LST. It allows them to retain full control over their financial strategy and branding while outsourcing the deep technical complexity to Sanctum’s proven liquidity layer and composable backend.

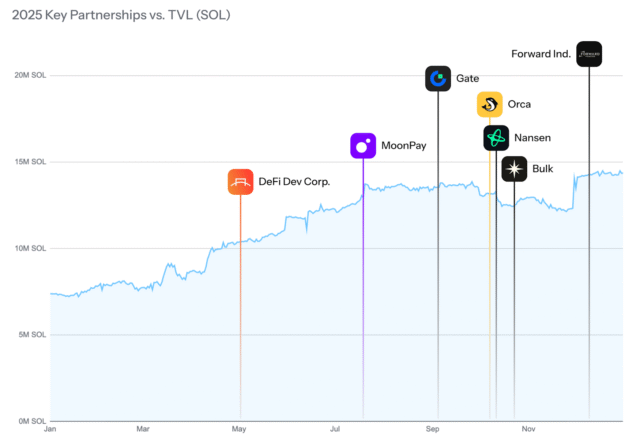

We are already seeing strong validation. In May 2025, DeFi Development Corp (NASDAQ: DFDV), a publicly traded financial firm, launched dfdvSOL using Sanctum’s infrastructure. This marked the first time a listed company held and utilized a bespoke Solana LST. Their explicit goal is to contribute liquidity back to the Solana DeFi ecosystem, creating a flywheel effect that also benefits their own corporate balance sheet.

Source: DeFillama

It is our core belief that as more structured SOL products emerge to compete for this new wave of capital, Sanctum will be their default launch partner and liquidity backbone.

Our thesis is clear. In the short to medium term, Sanctum is the most underrated infrastructure play for this institutional wave, and they are quietly becoming the essential plumbing every major yield-bearing Solana product will depend on.

Thesis #3: Sanctum App will become the de facto entry point for Solana

At the 2025 Solana Breakpoint, Sanctum unveiled its latest endeavor: the Sanctum App. This is a lightweight, delightful application designed to help users effortlessly grow their $SOL holdings through daily rewards in a fun, gamified environment.

This pivot stems from a first-principles approach. Referring back to our initial thesis, the primary reason Sanctum LSTs haven’t yet reached peak market penetration is the friction inherent in current DeFi UX. It is easy to forget that many $SOL holders exist entirely outside the “DeFi bubble.” They aren’t interested in the technical internals of Solana or the complex math behind LST yields; the only way to reach them is to abstract that complexity away. Following the massive success of Wonderland, we are doubling down on our belief that the Sanctum founding team is one of the few with the “DNA” to not only build a community but—more importantly—earn its lasting trust. From a team-gene perspective, we are confident they can capture lightning in a bottle once again.

From a product standpoint, the journey has come full circle. The Sanctum team were the pioneers who took the complicated concept of stake accounts and made LSTs accessible. Now, they are scaling that mission to a much wider audience. Moving forward, we expect the Sanctum App to serve as the primary interface and entry point for everyday users, while Sanctum LSTs continue to function as the foundational backbone of the entire Solana infrastructure.

Summary

When we look at Sanctum we see more than just a protocol, but the foundation of Solana’s next chapter: at its core is FP, a contrarian founder who builds with conviction and has led Sanctum from a simple idea into the liquidity fabric of Solana, and now it’s expanding even further into the transaction infrastructure. Apart from that, we also see the LST business continues to compound through strong network effects, institutional adoption, and deep integrations across the ecosystem.

Ultimately, this is why we invested. FP & Sanctum represent everything we believe in.

About AppWorks

Founded in 2009, AppWorks is a leading accelerator + VC in Asia and Web3, managing US$ 368M across its funds. At AppWorks, we invest in the founders who are obsessed with true product-market fit and committed to playing the long game. If this resonates with you, let’s chat.

從大學就開始創業,也讓他洞悉自己對於企業正規軍的策略理解不足。當他看到 LINE 要收購 Choco TV,覺得這是一個難得的機會,可以親身觀察國際公司是怎麼做併購與整合的。剛好 Choco TV 的創辦人 Davidd 也是Colorgy 的天使投資人,兩人相談合拍下,James 就加入整合團隊。參與了整個過程,從資料與技術對接、流程重新設計,到如何讓兩邊團隊建立共識、對齊預期。這段經歷讓他對大企業如何運作、如何協調文化落差有了第一手的理解,這些經驗也成為他日後共同創辦 MetaCRM、處理企業銷售與 B2B 合作的重要底氣。

James 能從零打造產品,也能在面對大型企業與通路夥伴時穩健談判,並且擁有實戰經驗:從一個大學生寫 App 的工程師、到主導國際產品落地、再到參與企業併購與跨部門整合,最後又成立 B2B SaaS 軟體新創。這些經驗讓 JTCG 能夠同時運作 PLG(product-led growth)與 SLG(sales-led growth)這兩種成長引擎,使其 AI 產品能快速打入市場並有效擴張。

解痛點、建資料飛輪,打造 AI 客服的持續競爭優勢

James 在經營 Zendesk 代理商期間,完整接觸企業客服流程,從大量客服工單與報表看見了兩個關鍵問題。第一,傳統規則式聊天機器人resolution rate (解決率,指顧客問題能被解決) 通常不到一成,而客服人力卻有七成時間進行重複「查詢系統資料、確認資料、回覆客戶」的工作;其二,多數國際大型客服 AI 工具雖功能強大,但價格昂貴且不夠接地氣,對本地語言與系統整合也缺乏彈性。這些觀察讓他意識到一個結構性機會:當地的 SI 可以造自己的 AI agent,取代國際 SaaS 工具,取代昂貴的國際 SaaS 預算,並提供更貼近需求的在地服務。

這些第一線經驗促成了 Raccoon AI 的誕生。機器人不僅能對話,更能直接喚用「查訂單、取消、退款」等後端 API,把客戶真正需要的動作一次完成。舉例來說,顧客詢問『我的訂單出貨了嗎?』時,Raccoon AI 不只回覆流程,而是會即時查詢電商後台的訂單管理系統,調出該訂單狀態,確認是否已出貨並提供物流單號,若尚未出貨還能進一步協助取消或改期。這是與傳統規則式聊天機器人最大不同,透過串接公司後台資料庫讓機器人有更多 context ,進而提高工單 resolution rate。

Raccoon AI 自推出以來在實際專案中展現出明顯差異化優勢。以台灣電商與旅遊業為例,系統可自動解決六成以上的客服工單,而同類 LLM chatbot 的平均 resolution rate 通常不及三成。這部分優勢來自於 Raccoon 長期累積的在地產業語料,例如電商常見的「出貨查詢」「修改地址」「訂單取消」等對話範式,甚至包含繁體中文語境下的客服語氣、商品分類邏輯與品牌風格調性,這些內容被整理成超過一百萬筆的向量知識庫,能讓 AI 在第一天上線就接近人類客服的回答品質。加上即將推出的 low code 客服流程編輯器(V2 版本,目前進入 Beta 測試階段),新客戶可在兩天內完成概念驗證,並預期在四週內完成正式上線。

每解決一張客服工單,系統會將意圖、回答與品牌語調回寫至該客戶專屬的向量知識庫,進一步優化客服機器人的涵蓋能力與回應品質。這種「資料飛輪」機制讓每家商戶的 AI 隨使用逐步成長,搭配 Raccoon 極短的導入時間,能快速開始累積語料、加速學習與優化,有效鞏固其 first mover advantage。