By Sophie Chiu, AppWorks Principal

Taiwan Equity Market: Huge, Liquid, and High Multiple

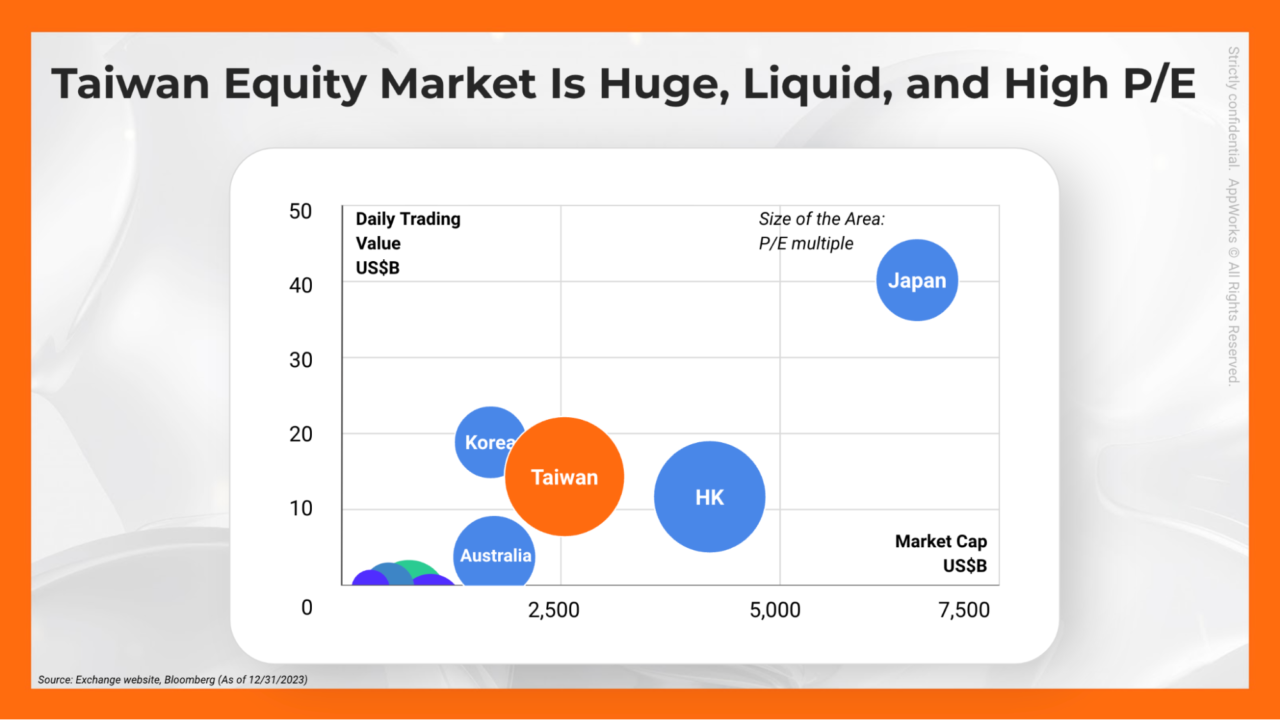

Taiwan’s equity market, with a market cap of US$2.6 trillion, ranks as the 4th largest in APAC, just behind China, Japan, and Hong Kong. It overshadows both Korea and Australia, standing at 4x the size of major equity markets in Southeast Asia.

While not the largest, Taiwan’s equity market has been the best-performing in the world this year, buoyed by strong fundamentals and investor sentiment around AI and related technology sectors. (For this, Bloomberg’s Editor-in-Chief wrote an article on 16-October about some of the fundamental supports behind the performance: Taiwan Outperforming World with Tech Halo.) This market boasts the highest trading turnover (US$15B daily) and valuation multiples (average P/E ratio of 22x) across Asia Pacific, supported by a tech-heavy composition, accounting for 60% of market cap. Such a density is the highest in Asia, whilst the next is Japan with merely 16%.

Meanwhile, the high retail participation, with 60% of trades by individual investors, also contributes to this vibrant market. It’s common for individuals to be highly informed, sometimes even more so than professionals, on company moves, like TSMC’s latest CAPEX plan, Tesla’s supply chain details, and which company would expand to Vietnam in the next quarter. Beyond retail, 30% of transactions come from foreign institutional investors, and 10% from local institutions, allowing a balanced investment thesis and trading momentum for the overall equity market.

A Liquid Choice For Small-Mid Cap

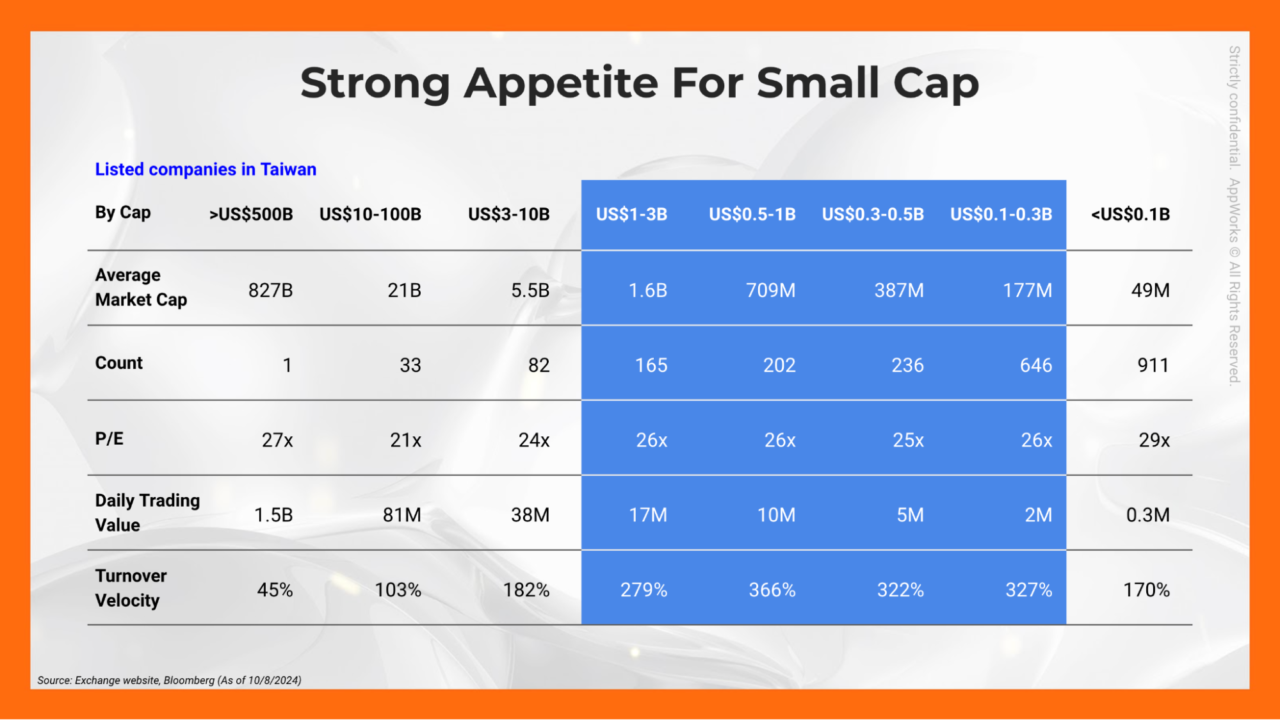

It is a market particularly good for small-mid cap companies with lower than US$10 billion market cap. In larger markets like Japan, where institutional investors make up 70% of trading, trading turnover tends to be lower. Having worked as an equity researcher and fund manager for ten years before joining AppWorks, I know institutional investors often avoid smaller stocks due to the “liquidity discount.” Taiwan, however, is an exception.

Taiwan’s market includes 2,200 stocks. Among them, 900 stocks are with caps below US$100 million and 1,200 are between US$100 million to US$3 billion. These companies don’t suffer from the liquidity discount and actually trade at higher P/E multiples than larger peers in the US$3-100 billion range. Their trading turnover is robust at 280-370%, meaning market cap turnover can reach 3-4 times per year.

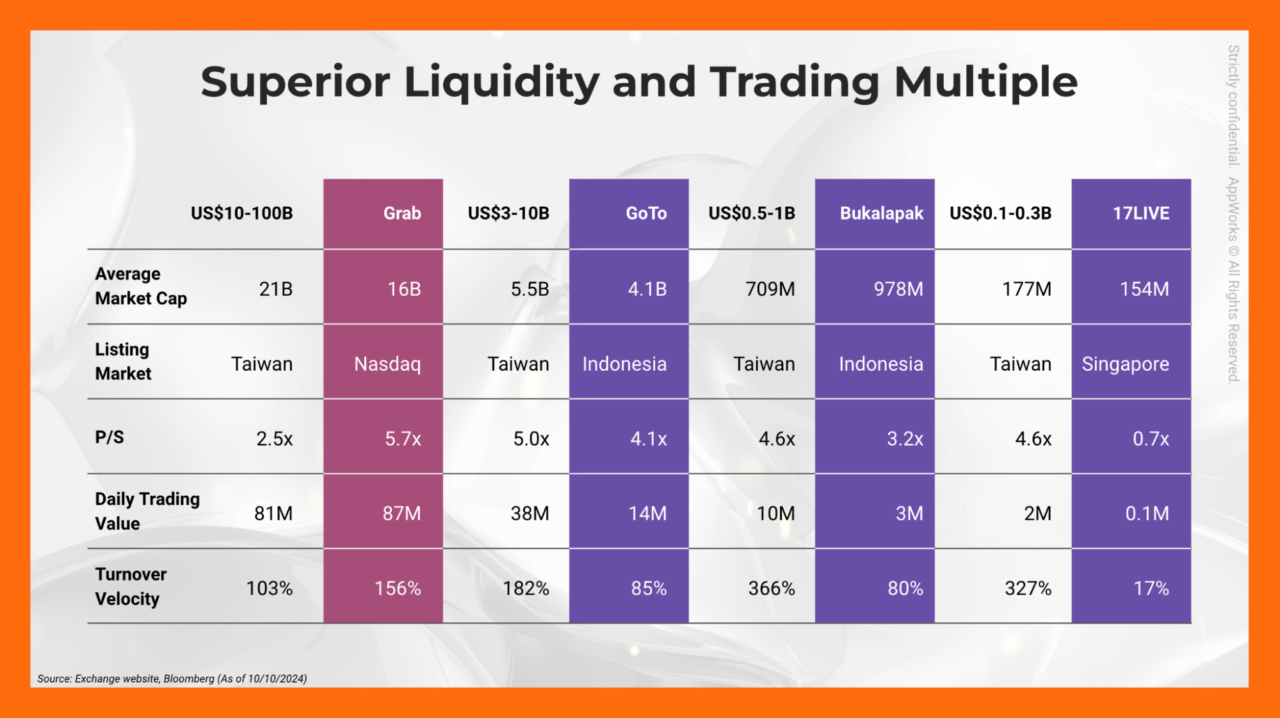

Comparatively, this liquidity advantage makes Taiwan a strong listing choice for companies from Southeast Asia. For companies the size of GoTo, Bukalapak, and 17LIVE, peer groups in Taiwan trade at higher P/S ratios and offer 3x (or even 20x in 17LIVE’s case) the daily liquidity. For a company like Grab, Taiwan’s trading volume is comparable at US$81 million daily, close to Nasdaq’s US$87 million.

A Long History of Welcoming Companies from Outside Taiwan

Encouraging Southeast Asian companies to list in Taiwan isn’t a new concept. Taiwan has long welcomed international companies, with strong investor interest in firms demonstrating overseas revenue and growth—an ideal fit for this small, export-driven island. After all, the majority of listed tech companies in Taiwan typically generate 70-100% of their revenue outside the country.

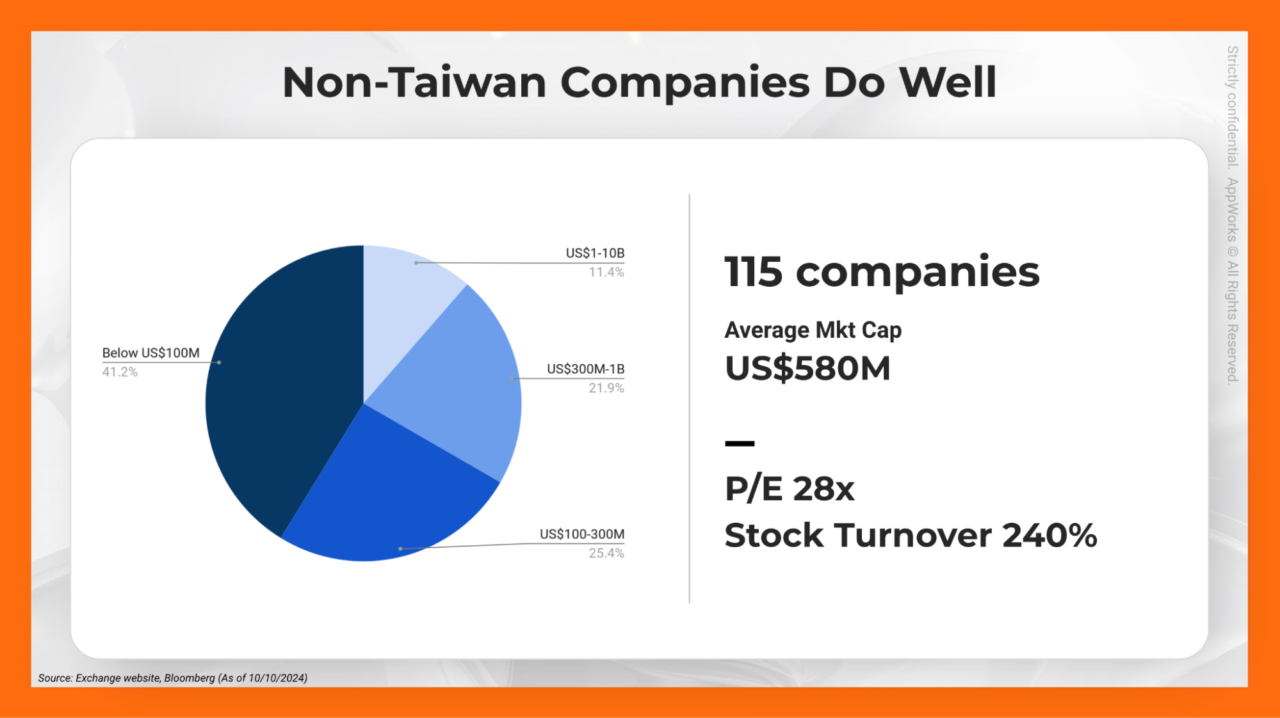

In 2009, Taiwan Stock Exchange (TWSE) allowed international companies to list, and today 115 such companies are listed here (in contrast, only 17 non-Japan companies are listed on the Tokyo Stock Exchange). Among them, 40% have caps below US$100 million, 50% between US$100 million and US$1 billion, and 10% exceed US$1 billion. These companies trade at an average 28x P/E with a 240% stock turnover, showing no discount for being not a Taiwanese company.

To promote the Taiwan market, AppWorks was invited by Startup Island Taiwan (a national startup ecosystem builder under the national fund) to host a panel with TWSE in Singapore on October 29 featuring Kelvin Wee, CEO of Patec (2236.TW), and May Kao, CFO of 91APP (6741.TW). 91APP is the first SaaS company listed in Taiwan, and Patec is a Singaporean company. Kelvin kindly shared why among all options, they chose to list in Taiwan where Patec has no operation, no business, no Taiwanese shareholders or family members, back in 2015.

As Kelvin shared, “Liquidity was the key reason. Taiwan’s equity market offers excellent liquidity, allowing our shareholders favorable trading conditions. As a Singapore company and a small cap, we didn’t consider the US. We thought about China as China was a big part of our revenues, but the stock market itself is more for its own domestic story and participation.”

Strong Support for New IPO and Post-IPO Fundraising

Kelvin further emphasized Taiwan’s unique post-IPO fundraising support: “After becoming a listed company, raising equity in Taiwan is straightforward. We can also issue zero-interest convertible bonds, repay with zero interest at maturity, or let them convert. This is very unique and probably only available in the Taiwan market.”

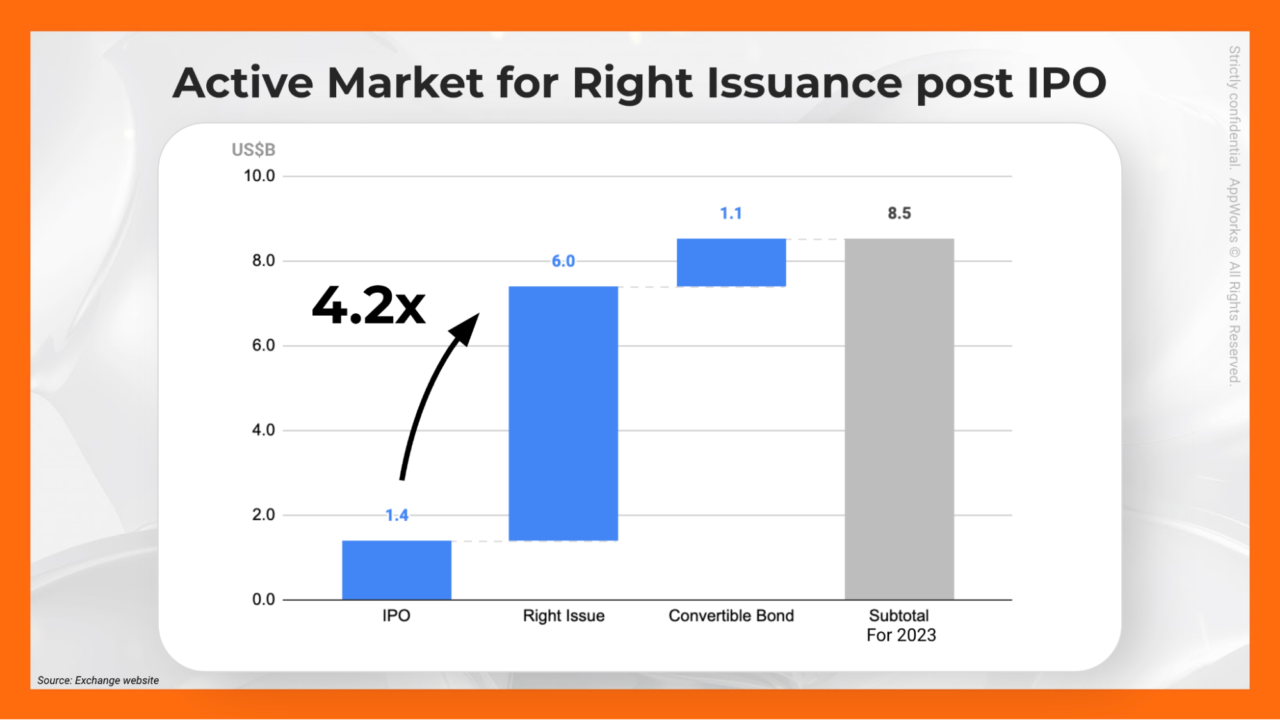

Indeed, in 2023, IPOs raised US$1.4 billion, and post-IPO equity raises amounted to US$6 billion, with convertible bonds reaching US$1.1 billion. This 5x secondary raise ratio is consistent year after year.

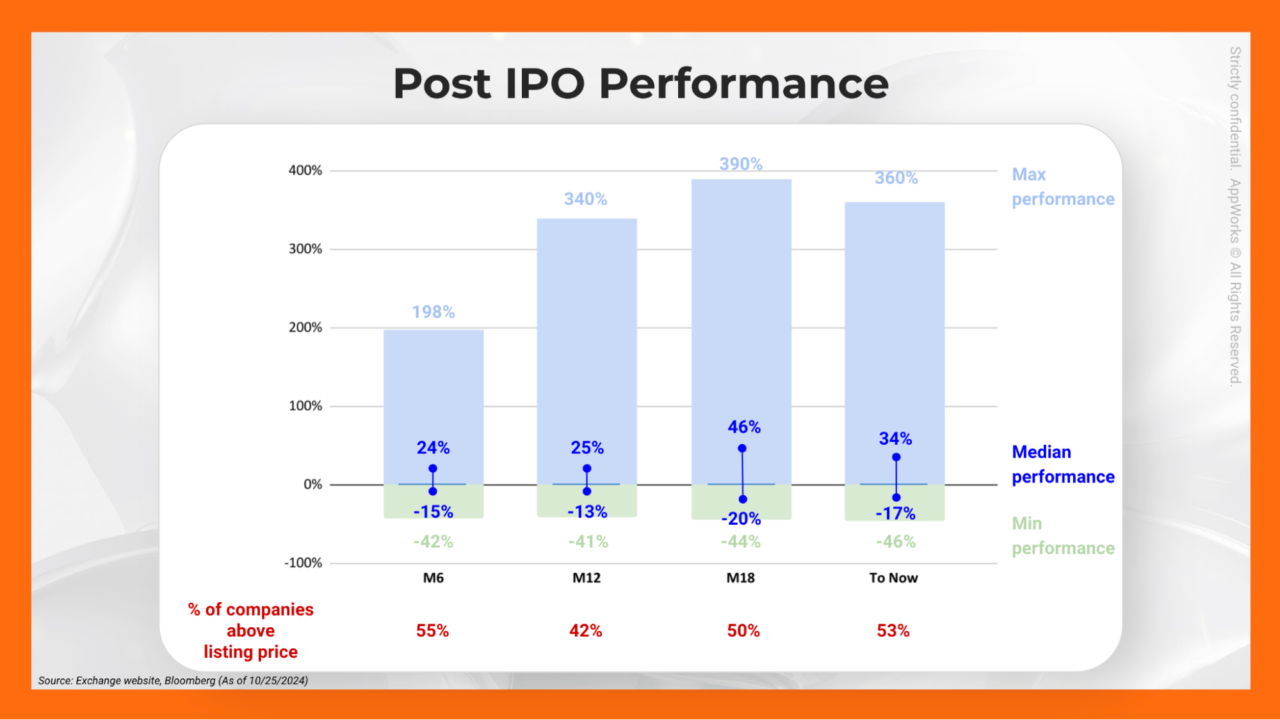

Unlike other markets where IPOs often underperform, Taiwan’s new IPOs tend to perform well, with 50% of IPOs since January 2023 (a total of 200 companies) still above their listing price after six months, and 42% and 55% at 12 and 18 months, respectively.

If we look deeper, those that stayed above the listing price could do 2-4x the stock performance the maximum, and up 24-46% the medium performance. Those that stayed below the listing price, they went down 40-45% the worst, with down 10-20% the median. It means, new IPO still tends to gain more and suffer less if we compare to other markets. For Grab, Goto, and Bukalapak, by the 18th month, the stock price went down 70-90%.

Join The Asian Nasdaq for Small-Mid Cap

The lackluster stock performance of Southeast Asian unicorns stems not only from their financial performance but also from the characteristics of their listing markets. Only mid-to-large-cap companies find it worthwhile to bear the effort and cost of listing in the U.S.—a path unsuitable for most Southeast Asian startups. Most Southeast Asian markets are still dominated by traditional industries, lacking a critical mass of tech stocks that would allow investors to benchmark and trade within, and justify the costs of coming to this market. Meanwhile, equity markets take decades to mature, shaped by economic growth and investor confidence, as well as stable currencies and favorable foreign investment policies to attract long-term institutional support. This is the allure of the mature market like Nasdaq and Taiwan. Taiwan’s equity market has taken 30 years to reach its current stage since the listing of TSMC and other rising tech companies.

We can proudly describe Taiwan’s equity market the “Asian Nasdaq for small-mid caps,” with a rich variety of tech sectors, including Semiconductor, Telecommunication, Electronic Distribution, Electronic Component, Electric Machinery, Computer, Software and System, Digital & Cloud, Fintech, Solar & GreenTech, and Biotech, among many others. This diversity allows tech companies clear sector positioning and benchmarking for investors.

Tech companies particularly benefit from Taiwan’s investor appetite for tech-centric investments. Taiwan offers high multiples, liquidity, funding access, and an understanding of tech companies’ intrinsic value—without penalizing them for being a small-mid cap or a non-Taiwan company.

Listing in Taiwan could offer an immediate remedy to the bleak exit prospects facing Southeast Asian tech startups. The favorable market dynamics in Taiwan might allow Southeast Asian unicorns to benefit from stronger investment interest and greater trading liquidity. With an improved exit outlook, VC investment in tech startups in this region could receive a much-needed boost, as it currently sits at a five-year low—or even a ten-year low if we consider only equity investments. The tech winter in Southeast Asia needs just a ray of sunlight to start melting the frozen investment confidence. Perhaps it’s time to look north.

Here below we show the listing threshold. For international companies, Taiwan’s listing requirements are very friendly, particularly with no need for operations, revenues or representatives in Taiwan, and a cost-effective, streamlined process. That’s an almost opposite approach with those from Tokyo Stock Exchange and Singapore Stock Exchange.

We hope more of you will join Taiwan’s tech landscape!

This article is done with great support from our IR Manager, Candice Su, and our wonderful AW#29 interns: Callista Harijanto, Jeremy Sutiono, and Lily Dai.